Introducing the 2018 annual reports of the European Court of Auditors

A word on the ‘2018 EU audit in brief’

The ‘2018 EU audit in brief’ provides an overview of our 2018 annual reports on the EU’s general budget and the European Development Fund, in which we present our statement of assurance as to the reliability of the accounts and the legality and regularity of the transactions underlying them. It also outlines our key findings regarding revenue and the main areas of spending under the EU budget and the European Development Fund, as well as findings relating to budgetary and financial management, the use of performance information, and follow-up of our previous recommendations.

The full texts of the reports may be found at www.eca.europa.eu or in the Official Journal of the European Union.

The European Court of Auditors (ECA) is the independent external auditor of the EU. We warn of risks, provide assurance, highlight shortcomings and good practice, and offer guidance to EU policymakers and legislators on improving the management of EU policies and programmes. Through our work we ensure that EU citizens know how their money is being spent.

|

President’s foreword

As the European Union’s external auditor, the ECA works with all EU institutions and bodies to help them manage the EU’s finances in a sound and economic manner.

This year, our annual report is published at an important crossroads in time. A new European Parliament was elected in May, and a new European Commission is to be appointed in November. The EU is in the process of agreeing its multiannual financial framework for 2021 to 2027. At the beginning of 2019, we issued ‘ECA remarks in brief’ summarising our main contributions on the Commission’s legislative proposals for the 2021-2027 spending period. These contributions are intended to assist the European Parliament and the Council make the necessary legislative changes so that in the years to come public money from the EU budget can be spent even more economically, efficiently and effectively.

In this year’s Statement of Assurance, as in previous years, we conclude that the EU accounts present a true and fair view of the EU’s financial position. Moreover, since the EU revenue we audited was not materially affected by error, we give a clean opinion on the regularity of the revenue side of the budget. At the same time, we issue a qualified opinion on the regularity of the transactions underlying the 2018 accounts, meaning that the errors identified through our audit work were not pervasive and therefore do not misrepresent the actual financial position of the EU. Our testing also shows that the overall level of irregularities in EU spending has remained within the range observed for 2016 and 2017. In addition, just like the last two years, a significant part of the expenditure we audited was not materially affected by error. This confirms the recent years’ sustained improvement in the management of the EU’s finances.

Thanks to improvements in its financial management, the European Union now meets high standards of accountability and transparency when it comes to spending public money. We need to build further on this success in improving the EU’s financial management in order to ensure that our citizens can maintain their trust in the EU and its Member States. In particular, we should jointly focus our scrutiny on areas where particular shortcomings persist and risks are particularly high. To this end, we at the ECA encourage all other EU institutions and bodies, particularly the new European Commission, to work together with us to further develop and harmonise our audit methodologies and practices.

Since the EU budget accounts for no more than about 1 % of the gross national income of all the Member States combined, it is vital that this EU spending not only complies with the rules, but also delivers results.

Klaus-Heiner LEHNE

President of the European Court of Auditors

Overall results

Key findings

Summary of the 2018 statement of assurance

The ECA gives a clean opinion on the reliability of the 2018 accounts of the European Union.

Revenue for 2018 was legal and regular, and free from material error.

Our opinion on expenditure for the financial year 2018 is qualified.

- Overall, the estimated level of error in expenditure from the 2018 EU budget was 2.6 %, which is within the range of error estimates for the last two years. For around half of the expenditure, the payments are made mainly based on entitlements, i.e. payments to beneficiaries for meeting certain conditions. For this type of spending we estimate the most likely level of error to be below the 2 % materiality threshold.

- This year – for the third year in a row – we issue a qualified opinion on payments as compared to an adverse opinion up to the year 2015.

- The European Commission’s regularity information sometimes differs from our findings. Its estimate of the levels of error are close to our estimates for ‘Competitiveness’ and ‘Natural resources’ and lower than ours in ‘Cohesion’.

- In 2018, there was a significant increase in payment claims for the European Structural and Investment (ESI) funds by Member States. At the same time, in the fifth year of the 2014-2020 multi-annual financial framework (MFF), the ESI funds absorption has continued to be slower than planned. This has contributed to increasing ESI funds outstanding commitments.

- Based on our analysis of selected programmes covering 97 % of the financial programming for the 2014-2020 MFF, we conclude that the performance indicators currently used for the EU budget do not always provide a good picture of actual progress made in achieving policy objectives.

- This year’s analysis of follow-up covered 184 recommendations issued in the 25 special reports published in 2015. Since then, the Commission has implemented 75 % of our recommendations fully or in most respects.

- We report all suspected fraud cases detected during our audit work to the EU’s anti-fraud office (OLAF). During 2018, we communicated to OLAF nine cases of suspected fraud.

The full text of our 2018 annual reports on the EU budget and on the activities funded by the 8th, 9th, 10th and 11th European Development Funds can be found on our website (eca.europa.eu).

What we audited

2018 EU budget in figures

The European Parliament and the Council adopt an annual EU budget, within the financial framework agreed for a multi-annual period. The current MFF period runs from 2014 to 2020. The Commission has the primary responsibility to ensure that the budget is properly spent.

In 2018, spending totalled €156.7 billion, the equivalent of 2.2 % of the total general government spending of EU Member States and 1.0 % of EU gross national income.

Where does the money come from?

The EU budget is financed by various means. In total, revenue amounts to €159.3 billion, of which the largest share (€105.0 billion) is paid by Member States in proportion to their gross national income. Other sources include customs duties (€20.2 billion), the contribution based on value-added tax collected by Member States (€17.1 billion) and, for example, contributions and refunds arising from Union agreements and programmes (€17.0 billion).

What is the money spent on?

The annual EU budget is spent on a wide range of areas. Payments are made to support activities as varied as farming and the development of rural and urban areas, transport infrastructure projects, research, training for unemployed people, support for countries wishing to join the EU, and aid to neighbouring and developing countries.

About two thirds of the budget is spent under what is known as ‘shared management’, with individual Member States distributing funds and managing expenditure in accordance with EU and national law (e.g. in the case of expenditure on ‘Cohesion’ and ‘Natural resources’).

Our statement of assurance on the EU budget

Every year, we audit EU revenue and expenditure, examining whether the annual accounts are reliable and whether income and expenditure transactions comply with the applicable rules at EU and Member State level.

This work forms the basis for our statement of assurance, which we are required to provide to the European Parliament and the Council under Article 287 of the Treaty on the Functioning of the European Union (TFEU). We examine expenditure at the point when final recipients of EU funds have undertaken activities or incurred costs, and when the Commission has accepted the expenditure. We did not examine pre-financed amounts unless they had been cleared in 2018.

Therefore, our audit population for 2018 amounted to €120.6 billion (see Figure 1).

Figure 1

2018 expenditure audited

This year, ‘Natural resources’ made up the largest share of our overall audit population (48 %), followed by ‘Cohesion’ (20 %) and ‘Competitiveness’ (15 %).

As last year, we examined ‘Cohesion’ based on the work of other auditors in the Member States and the Commission’s supervision. This means that our auditors reviewed and, if necessary, re-performed that work.

For more information on our audit approach, see chapter ‘Background information’.

What we found

EU accounts present a true and fair view

The 2018 EU accounts present fairly, in all material respects, the EU’s financial results and its assets and liabilities at the end of the year, in accordance with international public sector accounting standards.

We are therefore able to give a clean opinion on the reliability of (i.e. ‘sign off’) the accounts, as we have done every year since 2007.

Revenue for 2018 is legal and regular

We conclude that revenue is free from material error. Moreover, we examined selected revenue-related systems and assessed them as overall effective, with the exception of key internal controls for traditional own resources (TOR) at the Commission and in certain Member States which we found to be only partially effective.

EU expenditure is legal and regular, except for cost reimbursements

An error or an irregular payment is the amount of money that should not have been paid out from the EU budget, because it was not used in accordance with EU and/or national rules and thus does not comply either with what the Council and Parliament intended with the EU legislation concerned or with specific national rules in the Member States. We estimate the level of error statistically, basing on quantifiable (measurable in monetary terms) errors that we identified by testing a sample of transactions within the entire audited population of expenditure.

For expenditure as a whole, we estimate the level of error to be in the range of 1.8 % and 3.4 %. The mid-point of this range, the so-called most likely error, is 2.6 % (see Figure 2). This compares to 2.4 % in 2017 and 3.1 % in 2016.

Figure 2

Estimated level of error for the EU budget as a whole

Note:

We use standard statistical techniques to estimate the level of error. We are 95 % confident that the level of error for the population lies in the range between the lower and upper error limits (for more details, see Chapter 1, Annex 1.1 of the 2018 annual report).

The way EU funds are disbursed has an impact on the risk of error

Our 2018 audit results confirm our findings for 2016 and 2017: namely, the way expenditure is disbursed has an impact on the risk of error.

Errors were confined mainly to high-risk expenditure where payments from the EU budget are made to reimburse costs previously incurred by beneficiaries, and which can be subject to complex rules. Such cost reimbursements can be subject to complex eligibility conditions, which in turn may lead to errors. This type of expenditure accounted for around 51 % of our audit population in 2018 and the estimated level of error was 4.5 %. This compares to 3.7 % in 2017 and 4.8 % in 2016.

At the same time, the most likely error rate estimate for low-risk expenditure (which accounts for the remaining 49 % of our audit population and mainly includes entitlement-based payments) was below our materiality threshold of 2 % (see Figure 3).

Figure 3

About half of the 2018 expenditure audited was free from material error

We therefore conclude that error is not pervasive and that, with the exception of high-risk expenditure, 2018 payments were legal and regular.

What are entitlement and cost reimbursement payments?

EU spending is characterised by two types of expenditure involving distinct patterns of risk:

- entitlement payments, which are based on beneficiaries meeting certain (less complex) conditions: these include, for example, student and research fellowships (under ‘Competitiveness’), direct aid for farmers (‘Natural resources’) and salaries and pensions for EU staff (‘Administration’);

- cost reimbursements, where the EU reimburses eligible costs for eligible activities (involving more complex rules): these include, for example, research projects (under ‘Competitiveness’), investment in regional and rural development (‘Cohesion’ and ‘Natural resources’) and development aid projects (‘Global Europe’).

‘Natural resources’ had the largest share of audited expenditure (48 %). ‘Direct support’, consisting mainly of direct aid payments to farmers, accounted for 72 % of this area and was free of material error. ‘Rural development, market measures, the environment, climate action and fisheries’ is the other component of ‘Natural resources’. ‘Cohesion’, the second largest share of audited expenditure (20 %), was affected by material error, mainly due to the reimbursement of ineligible costs and infringements of internal market rules.

Our estimated level of error for ‘Competitiveness’ is lower than in 2016 and 2017, but still material. This year we found most errors in research expenditure, mainly due to beneficiaries overdeclaring costs, such as personnel costs, other direct costs, overheads or ineligible subcontracting costs.

‘Administration’ was free from material error. Most expenditure in this area takes the form of salaries, pensions and allowances paid by EU institutions and bodies.

Figure 4 compares the estimated levels of error in the various spending areas between 2016 and 2018. Further information on results in revenue and each spending area is given in the chapter ‘A closer look at revenue and spending areas’ and in the relevant chapters of the 2018 annual report.

Figure 4

Comparison between estimated levels of error for EU spending areas

Note:

The estimated level of error is based on quantifiable errors, which we identified through our work, notably the testing of a sample of transactions. We use standard statistical techniques to draw this sample and to estimate the level of error (see Chapter 1, Annex 1.1 to the 2018 annual report).

Comparison between the Commission’s estimate of the amount at risk at payment and our estimated level of error

In the context of the attestation approach for our statement of assurance, we compared our estimated level of error with the Commission’s estimate of the amount at risk at payment, which represents its estimate of the amount, at the moment of payment, that has not been paid in accordance with the applicable rules.

Each Commission Directorate-General (DG) produces an annual activity report. This includes a declaration in which the Director-General provides assurance that the report properly presents financial information and that transactions under his/her responsibility are legal and regular. All Directorates-General provided estimates of their levels of error, which are close to our estimated level of error for ‘Competitiveness’ and ‘Natural resources’ and lower than ours for ‘Cohesion’.

Overall, the Commission’s estimate of the amount at risk at payment for 2018 is 1.7 %. This is below our error estimate which is in a range between 1.8 % and 3.4 %.

We reported nine cases of suspected fraud to OLAF

Fraud is an act of deliberate deception to derive benefit. Our estimate of the level of error in the EU budget is therefore neither a measure of fraud nor of inefficiency or waste. Rather, it is an estimate of the money that should not have been paid out because it was not used in accordance with the applicable rules and regulations.

We report all suspected fraud cases detected during our audit work to the EU’s anti-fraud office OLAF, which then decides whether it will investigate and follow up these cases, where appropriate in co-operation with national judicial authorities. During 2018, we communicated to OLAF nine cases of suspected fraud

The instances of suspected fraud concerned the artificial creation of the necessary conditions for EU financing, the declaration of costs not meeting the eligibility criteria and procurement irregularities. Some of these suspected fraud cases involved several irregularities.

Want to know more? Full information on the main findings can be found in Chapter 1 of our 2018 annual report. The full text of our annual report can be found on our website (eca.europa.eu).

Budgetary and financial management faces challenges

Significant increase in claims for the ESI funds

In 2018, the EU used both commitment and payment appropriations almost entirely. Out of €160.7 billion available for commitments, €159.9 billion were used (99.5 %) and of the €144.8 billion available for payments, €142.7 billion were made (98.6 %).

The number of ESI funds claims in 2018, which account for around 43 % of the 2014-2020 MFF, has significantly increased. This is mainly because of the relatively low level of ESI fund payment claims by Member States in the early years of the 2014-2020 programmes.

Implementation of the MFF affected by delays in the implementation of ESI funds

Delays in the implementation of the ESI funds’ continue to affect the final years of this MFF. Payment claims for a substantial value have been delayed and will be submitted in future years. This has affected the use of pre-financing and outstanding commitments, and will affect payment appropriation needs at the start of the next MFF. We recommend that the Commission takes measures to avoid undue pressure on the level of payment appropriations in the first years of the

The absorption of ESI funds gained momentum in 2018, the fifth year of the current MFF. By the end of the year, on average only 27.3 % of total allocations for the whole MFF had been paid to the Member States, compared with 33.4 % by the end of 2011, the corresponding year of the previous MFF. The low absorption of ESI Funds has contributed to increasing ESI funds outstanding commitments.

Figure 5 shows each Member State’s ESI funds outstanding commitments, both as an amount in euros and as a percentage of its 2018 general government expenditure.

In our rapid case review on outstanding commitments in the EU budget, we highlight the significant risks that a high level of outstanding commitments can create for the EU budget and present possible solutions.

Figure 5

Outstanding commitments of ESI funds at the end of 2018

The increase in guarantees adds to the EU budget’s exposure to risk

Guarantees supported by the EU budget have increased in recent years, mainly due to the addition of the European Fund for Strategic Investments (EFSI) guarantee and the European Fund for Sustainable Development (EFSD) guarantee. In total, the actual guarantee exposure at the end of 2018 was €92.8 billion. This increases the EU budget’s exposure to risk. The level of losses expected by the Commission is covered by guarantee funds, which the new MFF will pool into a common provisioning fund.

We recommend that the Commission, as soon as the common provisioning fund is established, ensures the effective management and up-to-date monitoring of the EU budget’s exposure to the related guarantees, and bases its calculation of the effective provisioning rate on a prudent methodology based on recognised good practice.

The European Investment Bank – an integral part of the EU’s architecture, but different accountability arrangements

The European Investment Bank Group (the EIB Group) grants loans, guarantees and other kinds of support on a non-profit-making basis in order to serve EU policy objectives. At the end of 2018, the aggregate total of outstanding loans granted by the EIB Group was €536 billion (2017: €548 billion).

The EIB Group is not an EU institution. In order to take account of its special nature, it has different management and governance arrangements compared to the rest of the EU budget. In recent years, the EU has increasingly made use of financial instruments and budgetary guarantees provided to the EIB Group. This trend is expected to continue during the next MFF.

At present, our audit mandate does not cover EIB Group operations that are not financed by the EU budget but serve the same EU objectives. This means that the ECA is unable to provide a full picture of the link between EIB Group operations and the EU budget.

In our briefing paper on the future of EU finances, we proposed that we should also be invited to audit the EIB’s non-EU-budget-related operations. The European Parliament supported our proposal in its resolution on the Annual Report on the control of the financial activities of the EIB for 2017.

We recommend that the Commission provides the budgetary authority with relevant information to support its work on the scrutiny of the EIB Group and its operations while also increasing the transparency of such operations.

Want to know more? Full information on the main findings on budgetary and financial management can be found in Chapter 2 of our 2018 annual report.

Further emphasis on performance of the EU spending needed

Each year we analyse a number of aspects relating to performance, the results achieved by the EU budget, which is implemented by the Commission in cooperation with the Member States. This year we have looked specifically at the EU budget performance indicators, the main results from our 2018 special reports on performance and the implementation of the recommendations we made in the special reports we published in 2015.

Performance indicators show significant variation in achievements and suggest moderate progress overall

We reviewed the quantitative information provided by performance indicators. For our analysis, we selected 22 out of the 60 spending programmes, choosing the four programmes with the highest planned expenditure for each 2014-2020 Multiannual Financial Framework (MFF) heading, plus two programmes for special instruments. The 22 selected programmes covered 97 % of the financial programming for the seven-year period. We found that the indicators show significant variation in achievements and moderate progress overall. The late, slow start for both the cohesion and rural development programmes was an important limiting factor.

Indicators did not always provide a good picture of actual progress

Our analysis revealed weaknesses in the framework of EU budget performance indicators. Many indicators were not well chosen for instance because they did not measure the achievements of the EU budget or because they were mostly focused on inputs and outputs rather than results and impacts. Furthermore, progress could not be calculated for many indicators and when it could, the data available was sometimes of insufficient quality. As regards the targets we noted that a number of them are not sufficiently ambitious.

We made recommendations to the Commission in relation to the selection of indicators, the setting of targets, obtaining timely information and the reporting on achievements.

Thirty-five special reports across the different areas of EU spending published in 2018

In line with our 2018-2020 strategy, we have been increasing our focus on assessing performance in EU action. In our special reports, we examine whether the objectives of selected EU policies and programmes have been met, whether results have been achieved effectively and efficiently and whether the EU funding has added value – i.e. whether it has delivered more than could be achieved with actions at the national level alone.

Figure 6 presents all 35 special reports published in 2018.

Figure 6

Special reports published in 2018

Our special reports – which are mainly performance audits – are available in 23 EU languages on our website (eca.europa.eu).

The Commission implements a high proportion of our recommendations

We review annually the extent to which the Commission has taken corrective action related to our recommendations. In line with our strategy for 2018-2020, we will be following up all performance audit recommendations we made to the Commission three years earlier.

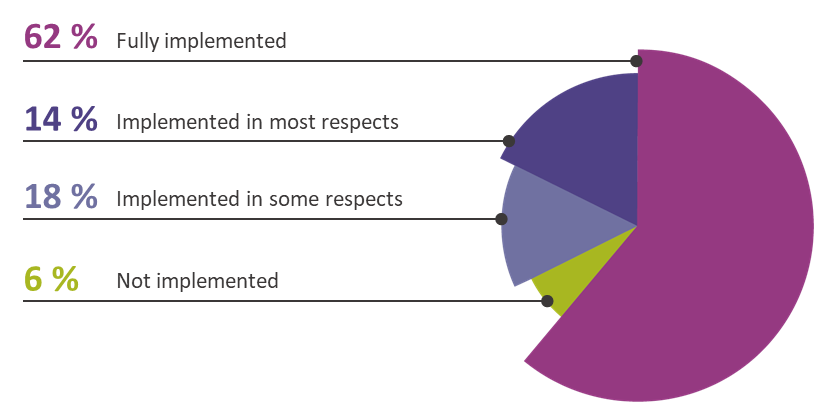

This year’s analysis of follow-up covered 184 recommendations issued in the 25 special reports published in 2015. The Commission has implemented 76 % of the recommendations fully or in most respects. We found that 11 recommendations had not been implemented at all (see Figure 7).

Figure 7

Three quarters of our recommendation issued in 2015 have been implemented fully or in most respect

Want to know more? Full information on the main findings on budgetary and financial management can be found in Chapter 3 of our 2018 annual report.

A closer look at revenue and spending areas

Revenue

€159.3 billion

What we audited

Our audit covered the revenue side of the EU budget, which finances the EU’s expenditure. We examined certain key control systems for managing own resources, and a sample of revenue transactions.

Contributions from Member States based on their gross national income (GNI) accounted for 66 % of the EU’s total revenue in 2018, while revenue from value added tax (VAT) accounted for 11 %. These contributions are calculated using macroeconomic statistics and estimates provided by Member States.

Traditional own resources (TOR), consisting mainly of customs duties on imports collected by Member State administrations on the EU’s behalf, provided a further 13 % of EU revenue. The remaining 10 % came from other sources (e.g. contributions and refunds arising from EU agreements and programmes, interest on late payments and fines, and other revenue).

What we found

| Amount subject to audit | Affected by material error? | €159.3 billion | No - Free from material error in 2018 and 2017 |

|---|

Preventive and corrective measures

Overall, the revenue-related systems we examined were effective, while the key internal TOR controls we assessed at the Commission and in certain Member States were partially effective.

We found that the Commission’s inspection plan was not sufficiently supported by a structured and documented risk assessment. This affected the Commission’s verification of the Member States’ TOR statements. We also found weaknesses in the Member States’ management of customs duties, in particular concerning the compilation of TOR statements, delays in enforcing recovery of customs debts and the late recording of such debts in the accounting system.

In addition, we noted that for the third year in a row, the Commission, in its annual activity report, had set a reservation regarding the accuracy of the value of TOR collected. This resulted from the evasion of customs duties on textile and footwear by some importers.

What we recommend

We recommend that the Commission:

- implement a more structured and documented risk assessment for its TOR inspection planning, including an analysis of each Member State’s level of risk and of risks in relation to the drawing up of the accounts on the customs duties;

- reinforce the scope of its monthly and quarterly checks of TOR statements by carrying out a deeper analysis of the unusual changes in order to ensure a prompt reaction to potential anomalies.

Want to know more? Full information on our audit of EU revenue can be found in Chapter 4 of our 2018 annual report.

Competitiveness for growth and jobs

Total: €21.4 billion

What we audited

Spending programmes in this policy area play an important role in stimulating growth and creating employment in the EU. The Seventh Framework Programme (FP7) and Horizon 2020 (H2020) for research and innovation, and Erasmus+ for education, training, youth and sport account for the bulk of expenditure. Other programmes provide funding for the space programme Galileo (the EU’s global satellite navigation system), the Connecting Europe Facility (CEF) and the International Thermonuclear Reactor.

For 2018, expenditure of €17.9 billion was subject to audit in this area. Most of that amount was directly managed by the Commission and took the form of grants to public or private beneficiaries participating in projects. Research and innovation programmes accounted for 45 % of the spending we audited in 2018.

What we found

| Amount subject to audit | Affected by material error? | Estimated most likely level of error | €17.9 billion | Yes | 2.0 % (2017: 4.2 %) |

|---|

In 2018, 54 of the 130 transactions we examined (42 %) were affected by errors. We estimate the most likely level of error to be 2.0 %. This figure is lower than in 2017, but still considered to be material.

Preventive and corrective measures

As in previous years, the principal risk to the regularity of transactions is that beneficiaries declare ineligible costs, which are neither detected nor corrected before the Commission reimburses them. We found that most errors related to ineligible costs (e.g. travel and equipment costs unconnected with the project), personnel costs not incurred directly for the project, and large research infrastructure costs wrongly declared by beneficiaries.

Example – multiple errors in a single claim

A small healthcare company participating for the first time in an EU project declared €1.1 million in personnel, subcontracting and other costs. The vast majority of the items we examined contained errors. In particular, the beneficiary did not use a method to calculate personnel costs in line with H2020 rules.

The Commission had applied corrective measures that directly affected four of the 130 transactions examined. Without these measures, our estimated level of error for this chapter would have been higher by 0.1 percentage point.

At the same time, sufficient information was available to prevent, or to detect and correct, eight other cases where we found, and quantified, errors. Had this information been used to correct the errors, the estimated overall level of error for spending on ‘Competitiveness for growth and jobs’ would have been 0.3 percentage point lower and thus below the materiality threshold.

Horizon 2020 and Erasmus+

We have previously reported that Horizon 2020 has simpler funding rules than its predecessor, FP7. In addition, under H2020, beneficiaries can declare capitalised and operating costs for large research infrastructure (LRI) if they comply with certain conditions and have first obtained a positive ex-ante assessment of their costing methodology from the Commission. However, this year’s audit showed that the ex-ante assessment had little impact on error prevention.

For H2020, we also reviewed audits carried out by both the Commission and contracted external auditors. In some of the files we reviewed, we found inconsistent sampling approaches and weaknesses in the documentation and reporting of audit findings, as well as in the quality of audit procedures. We also found a methodological weakness relating to the error rate calculation: although ex-post audits rarely achieve their aim of maximum coverage of accepted costs, the error rate is systematically calculated based on all accepted costs instead of the amount actually audited. This leads to an understatement of the error rate.

For Erasmus+, we note that, like last year, the Education, Audio-visual and Culture Executive Agency (EACEA) has issued a reservation concerning the effectiveness of its internal controls for managing grants. In addition, our audits of Erasmus+ projects showed that some national rules were not fully aligned with the principles applied by the EU, in particular as regards maximum amounts payable and funding arrangements.

Commission reporting on legality and regularity

The 2018 AAR of the Directorate-General for Research and Innovation (DG Research and Innovation), the EACEA and the Executive Agency for SMEs (EASME) gave a fair assessment of their financial management and the regularity of underlying transactions. Overall, the information they provided corroborated our findings and conclusions.

Performance assessment

We assessed the Commission’s reporting on the performance of 50 research and innovation projects in our sample. According to the progress reports for these projects, most of them had achieved the expected outputs and results. However, in some cases, the reported progress was only partly in line with the agreed objectives or the reported costs were disproportionate to the progress made. Furthermore, in some cases, the project outputs and results had not been disseminated as intended.

What we recommend

We recommend that the Commission:

- inform SMEs more effectively about the applicable funding rules and carry out more targeted checks of cost claims of SMEs; for the next Research Framework Programme, further simplify the rules for declaring personnel costs and large research infrastructure costs;

- for H2020, take measures to address the observations made on ex-post audits concerning sampling consistency, documentation and reporting of audit findings, as well as the quality of audit procedures; and

- promptly address the findings of the Commission’s Internal Audit service concerning:

- the EACEA’s internal control systems on the grant management process for Erasmus+; and

- the monitoring of compliance with contractual obligations and reporting requirements on dissemination and exploitation in research and innovation projects.

Want to know more? Full information on our audit of EU expenditure on ‘Competitiveness for growth and jobs’ can be found in Chapter 5 of our 2018 annual report.

Economic, social and territorial cohesion

Total: €54.5 billion

What we audited

Spending under this policy area focuses on reducing development disparities between the different Member States and regions of the EU and strengthening competitiveness. These objectives are implemented mainly through the European Regional Development Fund (ERDF), the Cohesion Fund (CF) and the European Social Fund (ESF), which involves the co-financing of multiannual operational programmes (OP) from which projects are funded.

The management of expenditure is shared by the Commission and the Member States. Within the Commission, the Directorate‐General for Regional and Urban Policy (DG Regional and Urban Policy) is responsible for implementing the ERDF and the CF, and the Directorate‐General for Employment, Social Affairs and Inclusion (DG Employment, Social Affairs and Inclusion) for the ESF.

In 2018, expenditure that was subject to our audit in this area amounted to €23.6 billion and was significantly higher than in 2017 (€8.0 billion).

We examine payments once expenditure has been incurred, recorded and accepted. In line with this approach the amount subject to audit for the 2018 annual report also included €16.5 billion worth of expenditure from previous years that the Commission had accepted or cleared in 2018. Payments made in 2018 amounting to €47.4 billion and relating to expenditure it had not yet accepted, were not part of our audit population.

What we found

| Amount subject to audit | Affected by material error? | Estimated most likely level of error | €23.6 billion | Yes | 5.0 % (2017: 3.0 %) |

|---|

Preventive and corrective measures

In 2018, we drew a statistically representative sample of 220 transactions which Member States audit authorities had already examined. We found and quantified 36 errors in these 220 transactions. The management and audit authorities in the Member States had not detected these errors. Taking account of the 60 errors that the audit authorities had found, and the financial corrections applied by programme authorities (amounting to a total of €314 million for the 2007-2013 and 2014-2020 programming period taken together), we estimate the level of error to be 5.0 %.

The number and impact of the errors we found indicate that weaknesses persist with regard to the regularity of the expenditure declared by managing authorities. Ineligible expenditures and projects contributed most to our estimated level of error, followed by infringement of internal market rules (such as public procurement and state aid) and the absence of essential supporting documents. Some of these errors were the result of complex national rules going beyond what the EU legislation requires (see box below).

Example: Complex national eligibility conditions

We found that the eligibility rules for an operational programme in Poland included a condition prohibiting the use of an EU grant if another entity was carrying out the same type of business activity in the same premises. This requirement, which goes beyond what is set out in the EU regulations, was repeated in the grant agreement. As one beneficiary, a lawyer, set up its activity in the same premises as another legal firm, the project was ineligible for co-financing.

Assessment of the work of audit authorities

Audit authorities are set up to oversee the use of EU funds. Their work is a critical part of the assurance and control framework in Cohesion. This year we assessed the work of 15 out of the 126 audit authorities in 14 Member States in relation to 15 assurance packages for the 2014-2020 period and nine closure packages for the 2007-2013 period.

Similar to last year, in several cases, our review of audit authorities’ work revealed shortcomings relating to the scope, quality and/or documentation of their work and the representativeness of their sampling. All audit authorities in our sample had reported a residual error rate below 2 %. Following its verifications, the Commission corrected the residual error rate to be above 2 % for four out of the 15 assurance packages for the 2014-2020 period in our sample.

Because of the additional errors we detected, our recalculated rate was above 2 % for another four of the 15 assurance packages for the 2014-2020 period and one of the nine closure packages for 2007-2013.

The Commission’s assurance work and its reporting of the residual error rate in its annual activity reports

Annual activity reports (AARs) are the Commission’s key tool for reporting whether it has reasonable assurance that the control procedures put in place ensure the regularity of expenditure.

Last year, we pointed out that the reporting requirements for AARs had not been sufficiently adapted to the 2014-2020 control and assurance framework. Since then, the Commission has made efforts to improve its arrangements for reporting on regularity. In its 2018 AARs, the Commission updated its key performance indicator (KPI) on regularity and reported that the residual error rate for the 2016/2017 accounting year was below 2 % for both DGs.

However, we identified issues that affect the reliability of these figures. To this end, we reported that these rates are not yet final when the Commission publishes them and that they can only be considered to be minimum error rates .

In its Annual Management and Performance Report for the EU budget (AMPR) the Commission estimates that the amount of risk at payment for the 2018 relevant expenditure in the area of ‘Economic, social and territorial cohesion’ is 1.7 %. However, this figure includes expenditure, which has not yet gone through the full control cycle. This will only happen as from 2020.

We also identified a number of issues that could affect the closure of OPs from the 2014-2020 programming period with a final residual error rate below 2 %.

Our work on the different elements of our audit shows that the error rates for ‘Economic, social and territorial cohesion’ presented in the Commission’s 2018 AMPR and AARs currently can still not be relied upon.

Performance assessment

In 2018, we examined whether Member States set up output and result indicators in their OPs that were relevant to their objectives and whether the output and result objectives specified for projects corresponded to the OP objectives. We also examined whether Member States had set up a database with information on performance at project level and to what extent audit authorities checked the reliability of that information.

Although Member States have monitoring systems to record information on performance, we found a number of cases where authorities had not set result or output indicators at project level, and few cases where there were no indicators or targets at all with which to measure project performance. Furthermore, we found that completed projects have not always fully achieved their performance objectives.

What we recommend

We highlighted that four of our recommendations from last year concern issues that we found again and have therefore not been repeated. In addition we identified new issues and recommend that the Commission:

- ensure that regular checks, based on a representative sample of disbursements to final recipients, are carried out at the level of financial intermediaries either by the audit authority or by an auditor selected by the EIB Group;

- develop and implement appropriate control measures to prevent the possibility of material irregular expenditure at closure, where the regular checks were found to be insufficient;

- take the necessary steps to ensure that the checklists used by managing and audit authorities include verifications of compliance with article 132 of the Common Provisions Regulation, which states that beneficiaries must receive the total amount of eligible expenditure due no later than 90 days from the submission of the related payment claim; and

- address weaknesses identified at closure, and ensure that no programme can be closed with a material level of irregular expenditure.

Want to know more? Full information on our audit of EU expenditure for ‘Economic, social and territorial cohesion’ can be found in Chapter 6 of our 2018 annual report.

Natural resources

Total: €58.0 billion

What we audited

This spending area covers the common agricultural policy (CAP), the common fisheries policy, and part of EU spending on the environment and climate action.

The CAP accounts for 98 % of spending on ‘Natural resources’. Its three general objectives set in EU legislation are:

- viable food production, with a focus on agricultural income, agricultural productivity and price stability;

- the sustainable management of natural resources and climate action, with a focus on greenhouse gas emissions, biodiversity, soil and water; and

- balanced territorial development.

The Commission, in particular the Directorate-General for Agriculture and Rural Development (DG Agriculture and Rural Development), shares management of the CAP with paying agencies in the Member States. CAP spending falls into three broad categories:

- direct payments to farmers, which are fully funded by the EU budget;

- agricultural market measures, also fully funded by the EU budget, with the exception of certain measures co-financed by the Member States, such as promotion measures and the school fruit, vegetable and milk scheme; and

- Member States’ rural development programmes, co-financed by the EU budget.

For 2018, expenditure of €58.1 billion was subject to audit in this area.

What we found

| Amount subject to audit | Affected by material error? | Estimated most likely level of error | €58.1 billion | Yes | 2.4 % (2017: 2.4 %) |

|---|

Direct payments as a whole were free from material error

Direct payments to farmers are mainly based on the area of agricultural land declared by farmers. These payments account for 72 % of spending under the MFF heading ‘Natural resources’.

The main management tool for direct payments is the Integrated Administration and Control System (IACS), which incorporates the Land Parcel Identification System (LPIS). IACS has helped to bring down the level of error in direct payments, with the LPIS making a particularly significant contribution.

We checked 95 direct payments and found that 77 were unaffected by error. We conclude that direct payments, as a whole, were free from material error.

Rural development, market measures, fisheries, environment and climate action

Complex eligibility conditions increase the risk of error in these spending areas. We tested 156 payments and found that 40 were affected by error. The main sources of error were:

- ineligible beneficiaries, activities or costs (see example);

- the provision of inaccurate information on areas or animal numbers;

- non-compliance with procurement or grant award rules; and

- administrative errors.

Example: A beneficiary failed to comply with the eligibility rules for on-farm investments

We examined a case where a beneficiary, together with other family members, submitted a joint application for support to construct a pigsty, with capacity for up to 600 sows. Each of the joint beneficiaries applied for the maximum level of support, which was around €215 000. Since the purpose of the measure was to support the development of small and medium-sized farms, the eligibility conditions stipulated that applicants’ holdings must have neither an economic size above €250 000 nor an area greater than 300 hectares. The beneficiaries claimed to operate independent businesses. We found that they held shares in a family company operating on the same site. When taking into account the beneficiary’s share of the family company, his holding exceeded the ceiling for economic size.

Preventive and corrective measures

The Commission and the Member States’ authorities had applied corrective measures that directly affected 53 of the 251 transactions examined. Without these measures, our estimated level of error for this chapter would have been higher by 0.6 percentage point. At the same time, in 12 cases of quantified error, the national authorities had sufficient information to prevent, or to detect and correct, the error before declaring the expenditure to the Commission. Had the national authorities made proper use of all the information at their disposal, the estimated level of error would have been 0.6 percentage point lower.

Directorate-General for Agriculture and Rural Development’s reporting on regularity of CAP spending

DG Agriculture and Rural Development uses national control statistics it receives from the paying agencies. It also makes adjustments based on the results of the certification bodies’ audits, and on its own checks and professional judgement, to arrive at an estimation of the amount at risk at payment.

The director of each of the 76 paying agencies provides DG Agriculture and Rural Development with an annual management declaration on the effectiveness of their control systems and a report on the paying agency’s checks. Since 2015, in order to provide additional assurance, the certification bodies have been required to give an annual opinion for each paying agency on the legality and regularity of the expenditure for which the Member States have requested reimbursement.

DG Agriculture and Rural Development’s checks identified shortcomings in the certification bodies’ work. As we noted last year, continued improvement in the certification bodies’ work is required if the Commission is to use their work as its primary source of assurance on the regularity of CAP spending.

Based on their paying agencies’ control statistics, Member States reported an overall level of error close to 1 % for CAP spending as a whole. We reviewed DG Agriculture and Rural Development’s adjustments to Member State error rates. As in previous years, DG Agriculture and Rural Development based most of its adjustments on its own checks of paying agency systems and spending. DG Agriculture and Rural Development calculates the majority of these adjustments as flat rates, intended to reflect the significance and extent of weaknesses it identified in control systems.

DG Agriculture and Rural Development’s AAR estimates the amount at risk at payment at around 2.1 % for CAP spending as a whole and at around 1.8 % for direct payments. The Commission also presents these results in its AMPR. The Commission’s estimate is consistent with our conclusion indicating a material level of error for ‘Natural resources’ spending as a whole, but not for direct payments.

Performance assessment

We reviewed 113 sampled rural development actions in 18 Member States. We found that most actions had produced the expected outputs and that Member States generally checked the reasonableness of costs, but had made little use of simplified cost options.

We examined the Commission and Member States’ performance measurement and reporting under the CAP common monitoring and evaluation framework (CMEF). We focused on their use of result indicators for 113 rural development payments and 95 direct payments.

In line with the findings of our previous audits on performance measurement in agricultural and rural development spending, we identified several weaknesses in the way in which the Commission and Member States had applied the CMEF result indicators to measure and report on the performance of spending.

In the proposal to introduce a performance-based delivery model for the CAP for post-2020 period, the Commission defined common output, result and impact indicators. In our opinion No 7/2018 on the proposal, while we welcomed the shift to a performance-based model, we found that these indicators were not yet fully developed and made specific comments on the proposed indicators.

What we recommend

In our 2017 annual report, we made three recommendations to the Commission with a target implementation date end of 2019. They were related to the Member States’ actions to address the causes of errors and the quality of the work of certification bodies. These recommendations are also relevant to this year’s findings and conclusions, and we will follow them up in due course.

This year, we also recommend that the Commission, for the post-2020 period, take into account the weaknesses we identified in the current framework, in order to ensure that result indicators properly measure the effects of actions and that they have a clear link to the related interventions and policy objectives.

Want to know more? Full information on our audit of EU expenditure on ‘Natural resources’ can be found in Chapter 7 of our 2018 annual report.

Security and citizenship

Total: €3.1 billion

What we audited

This spending area groups various policies whose common objective is to strengthen the concept of European citizenship by creating an area of freedom, justice and security without internal borders.

‘Migration and security’ is largely implemented through shared management between the Member States and the Commission’s Directorate-General for Migration and Home Affairs (DG Migration and Home Affairs). The most important funds under this heading are:

- the Asylum, Migration and Integration Fund (AMIF) which aims to contribute to the effective management of migration flows and bring about a common EU approach to asylum and immigration;

- the Internal Security Fund (ISF), which aims to achieve a high level of security in the EU.

These funds began in 2014, when they replaced the SOLID programme (‘Solidarity and Management of Migration Flows’), and will run until 2020. In 2018, they account for around half (45 %) of EU spending in this area.

Spending by 13 decentralised agencies that are active in the implementation of key EU priorities in the areas of migration and security, judicial cooperation and health accounts for another 27 %. We report separately on EU agencies in our specific annual reports and an annual summary ‘Audit of EU agencies in brief‘.

For 2018, the expenditure subject to audit in this area was €3.0 billion.

What we found

In 2018, we reviewed selected systems covering the main policies of this spending area and examined a small number of transactions. We found DG Migration and Home Affairs’ management of calls for proposals and grant applications to be effective. At the same time, our examination revealed deficiencies in the application of public procurement rules, and some system weaknesses in the management of AMIF and the ISF and in the controls of the Food and Feed programme by the Directorate-General for Health and Food Safety.

What we recommend

We recommend that the Commission:

- ensure that, when making administrative checks of payment claims, it systematically uses the documentation it has required from grant beneficiaries to properly examine the legality and regularity of the procurement procedures these beneficiaries have organised; and

- instruct the Member State authorities responsible for national AMIF and ISF programmes to adequately check the legality and regularity of the procurement procedures organised by beneficiaries of the funds when making administrative checks of their payment claims.

Want to know more? Full information on our audit of EU expenditure for ‘Security and citizenship’ can be found in Chapter 8 of our 2018 annual report.

Global Europe

Total: €9.5 billion

What we audited

This spending area covers expenditure in the fields of foreign policy, the promotion of EU values, support for EU candidate and potential candidate countries, and development assistance and humanitarian aid for developing and neighbouring countries (with the exception of the European Development Funds which can be found in the relevant chapter).

Spending is implemented either directly by a number of Directorates-General at the Commission (either from their headquarters in Brussels or through EU delegations in more than 150 recipient countries), or indirectly by beneficiary countries and international organisations, using a broad range of cooperation instruments and delivery methods.

For 2018, the expenditure subject to audit in this area was €8.0 billion.

What we found

In 2018, we found some cases of ineligible expenditure and non-compliance with the legal and financial rules for awarding contracts, but we also came across examples of effective external controls.

The uncooperativeness shown by international organisations in not forwarding essential supporting documents seriously delayed our audit work. We consider that this constitutes an infringement of our audit rights under the Treaty on the Functioning of the EU.

Annual activity reports and other governance arrangements

In 2018, the Directorate-General for European Neighbourhood Policy and Enlargement Negotiations commissioned its fourth annual residual error rate (RER) study from an external contractor. The purpose of the RER study is to measure ‘errors that have evaded all prevention, detection and correction controls’. However, in 2018, for around 24 % of the sampled transactions, the RER relied fully on the results of previous controls, without any additional checks. This share had almost doubled since 2017.

Moreover, our review showed that there is scope for improving the degree of judgement allowed to auditors when estimating error for individual transactions.

The Directorate-General for European Civil Protection and Humanitarian Aid Operations has made additional efforts to exclude recoveries on pre-financing, cancelled recovery orders and earned interest from the calculation of the estimated amount at risk. We found nevertheless that the reliability of the 2018 figure presented in the DG's AAR was impaired by undetected errors that led to an overstatement of the DG’s corrective capacity.

Performance assessment

In addition to checking regularity, we assessed performance aspects for 15 completed projects. All but one of the projects we examined had clear and relevant performance indicators. Logical frameworks were well structured, and output objectives were realistic and achievable.

What we recommend

We recommend that the Commission:

- take all the necessary steps to reinforce the obligation on international organisations to provide us with any document or information we need for our work;

- take steps to adapt DG European Neighbourhood Policy and Enlargement’s methodology to limit full-reliance decisions, and that it monitors its implementation closely;

- amend the way corrective capacity is to be calculated in 2019 by excluding recoveries of unspent pre-financing.

Want to know more? Full information on our audit of EU expenditure for ‘Global Europe’ can be found in Chapter 9 of our 2018 annual report.

Administration

Total: €9.9 billion

What we audited

Our audit covered the administrative expenditure of the EU institutions and certain other bodies: the European Parliament, the European Council and the Council of the European Union, the Commission, the Court of Justice, the Court of Auditors, the Economic and Social Committee, the Committee of the Regions, the European Ombudsman, the European Data Protection Supervisor, and the European External Action Service.

In 2018, the institutions and bodies had a total of 9.9 billion euros in administrative expenditure. This amount comprised spending on human resources (about 60 % of the total), buildings, equipment, energy, communications and IT.

We publish the results of our audits of the EU agencies, other decentralised bodies and the European Schools separately, in specific annual reports. We also publish a consolidated summary of these audits.

An external auditor audits our own financial statements. The audit opinion and report are published in the Official Journal of the European Union and on our website.

For 2018, the expenditure subject to audit in this area was €9.9 billion.

What we found

| Amount subject to audit | Affected by material error? | €9.9 billion | No - Free from material error in 2018 and 2017 |

|---|

In 2018, we examined 45 transactions in this area of the budget. As in previous years, we estimated that the level of error is below the materiality threshold. However, this year we detected a greater number of internal control weaknesses at the Commission in its management of family allowances payable to staff.

Procurement procedures to improve the security of people and premises

In response to the spate of terrorist attacks in recent years, the EU institutions have adopted measures to strengthen the protection of their staff and premises as a matter of urgency. We examined 13 procurement procedures relating to these measures and organised by the institutions between 2015 and 2018. We focused in particular on the definition of needs, the nature of the procurement procedure used, the implementation of the procedure and the selection of contractors. We found weaknesses, usually tied to the urgency of concluding contracts, in procedures organised by the Parliament and by the Commission.

What we recommend

We recommend that the Commission:

- improve its systems for managing statutory family allowances. It should reassess staff members’ personal situation more frequently and strengthen its checks on the declaration of allowances received from other sources.

Want to know more? Full information on our audit of EU expenditure for ‘Administration’ can be found in Chapter 10 of our 2018 annual report.

European Development Funds

Total: €4.1 billion

What we audited

The European Development Funds (EDFs) are the main instrument by which the EU provides development cooperation aid. EDF spending and cooperation instruments aim to overcome poverty and to promote sustainable development and the integration of the African, Caribbean and Pacific (ACP) countries and overseas countries and territories (OCTs) in the world economy.

For 2018, expenditure subject to audit in this area was €3.7 billion. This expenditure relates to the 8th, 9th, 10th and 11th EDF.

What we found

The 2018 accounts present fairly the financial position of the EDFs, the results of their operations, their cash flow and changes in net assets.

We also conclude that the revenue of the EDFs was free from material error.

| Amount subject to audit | Affected by material error? | Estimated most likely level of error | €3.7 billion | Yes | 5.2 % (2017: 4.5 %) |

|---|

In 2018, we examined a representative sample of 125 transactions drawn from the full range of payments from the EDFs. Since part of this expenditure was covered by the residual error rate (RER) study made by Directorate-General for International Cooperation and Development (DG International Cooperation and Development), we included 14 further transactions in our sample, to which we applied, after adjustment, the results of this study. On the basis of the 39 errors we have quantified, and the adjusted results of the 2018 RER study, we estimate the level of error to be 5.2 %.

We found that most errors related to non-compliance with procurement rules, expenditure that either had not been incurred or was ineligible, overheads claimed as direct costs, and the absence of supporting documents.

For some transactions implemented by international organisations, they did not forward essential supporting documents within a reasonable time frame. This had a negative impact on the planning and execution of our audit work and goes against the Treaty on the Functioning of the EU, which establishes the ECA’s right to be sent the information it requests.

Example: Procurement error

The Commission concluded a contribution agreement with an international organisation to support public finance management in Jamaica. The total contract value and EU contribution was €5 million. When procuring supplies (€193 700) for the project, the organisation considered only its member countries as eligible suppliers. This excluded several countries, including some EU Member States, which should be eligible for EDF-funded projects.

Preventive and corrective measures

For a number of transactions containing quantifiable errors, the Commission had sufficient information to prevent or to detect and correct the errors. Had the Commission made proper use of all the information at its disposal, the estimated level of error for expenditure for the EDFs would have been 1.3 percentage point lower.

Compliance reporting by the Directorate-General for International Cooperation and Development

We reviewed the 2018 RER study contractor’s work. For the third year in a row, the study estimated the residual error rate to be below the 2 % materiality threshold set by the Commission. The RER study does not constitute an assurance engagement or an audit. As in previous years, we have identified limitations, such as the limited number of on-the-spot checks, the incomplete checks on public procurement procedures and calls for proposals, and the estimation of errors. All these limitations contributed to a lower RER, which does not reflect reality.

In its 2018 AAR, DG International Cooperation and Development issues two reservations: one concerning grants and one concerning specific programmes managed by the African Union Commission. The first reservation relates only to grants managed by the DG Neighbourhood and Enlargement Negotiations on behalf of DG International Cooperation and Development, as the reservation’s scope has been progressively tightened since 2016. Considering the limitations of the RER study in 2018 and in previous years, the narrow scope of the first reservation is not sufficiently justified. As the RER study is one of the key elements in DG International Cooperation and Development’s risk assessment, it needs to be supported by sufficiently detailed guidance in order to provide a reliable basis for the reservation.

DG International Cooperation and Development estimated the overall amount at risk at closure to be €49.8 million. Based on the RER study, this estimate is 29 % down on the previous year. Based on our observations on the RER study, we consider that the amount at risk should be higher.

Performance assessment

In addition to checking regularity, our on-the-spot checks allowed us to make observations on performance aspects for selected transactions. We noted cases where items purchased for EDF-funded measures were not being used, or installation works not carried out, as planned. These cases compromised the efficiency and effectiveness of the EU action.

Example: Project sustainability endangered

The Commission endorsed a works contract for the construction of a desalination plant in Djibouti. During our on-the-spot checks, we found that the area originally set aside for the project had been substantially reduced, and a new port and military base were being built instead in the immediate proximity of the desalination plant. The construction works and subsequent operation of the port and the military base may affect maritime currents, water quality and the location of water intake valves. All these factors could have a significant impact on the viability of the desalination plant, threatening its long-term sustainability.

What we recommend

We recommend that the Commission:

- take steps to reinforce the obligation on international organisations to forward to us, at our request, any document or information we need to carry out our work;

- improve the RER study methodology and manual so that they give more comprehensive guidance on the issues we have identified in this report, and therefore provide appropriate support for DG International Cooperation and Development’s risk assessment for the reservations;

Want to know more? Full information on our audit of EDFs can be found in the 2018 annual report on the activities funded by the 8th, 9th, 10th and 11th European Development Fund.

Background information

The European Court of Auditors and its work

The European Court of Auditors (ECA) is the independent external auditor of the European Union. We are based in Luxembourg and employ around 900 professional and support staff of all EU nationalities.

Our mission is to contribute to improving EU administration and financial management and to promote accountability and transparency, and act as the independent guardian of the financial interests of EU citizens.

Our audit reports and opinions are an essential element in the EU accountability chain. They are used to hold to account those responsible for implementing EU policies and programmes: the Commission, other EU institutions and bodies, and administrations in Member States.

We warn of risks, provide assurance, indicate shortcomings and good practice, and offer guidance to EU policymakers and legislators on how to improve the management of EU policies and programmes. Through our work, we ensure that Europe’s citizens know how their money is being spent.

Our output

We produce:

- annual reports, mainly containing the results of financial and compliance audit work on the EU budget and the European Development Funds, but also on budgetary management and performance aspects;

- special reports, presenting the results of selected audits on specific policy or spending areas, or on budgetary or management issues;

- specific annual reports on the EU’s agencies, decentralised bodies and joint undertakings;

- opinions on new or updated laws with a significant impact on financial management – either at the request of another institution or on our own initiative;

- review-based publications, providing a description of, or information about, policies, systems, instruments or more focused topics.

Finally, our audit previews present background information on a forthcoming or ongoing audit task.

Audit approach for our statement of assurance at a glance

The opinions in our statement of assurance are based on objective evidence obtained from audit testing in accordance with international auditing standards.

As stated in our 2018-2020 strategy, we aim to apply the attestation approach to our entire statement of assurance, meaning that we would base our audit opinion on the Commission’s (management) statement. This has been the case for our work on the reliability of accounts since 1994. Where the terms of the relevant international auditing standards have been met, we review and re-perform the checks and controls carried out by those responsible for implementing the EU budget. We thus take full account of any corrective measures taken on the basis of these checks.

Reliability of the accounts

Do the EU annual accounts provide complete and accurate information?

Hundreds of thousands of accounting entries are generated by Commission Directorates-General each year, taking information from many different sources (including Member States). We check that accounting processes work properly and that the resulting accounting data are complete, correctly recorded and properly presented in the EU’s financial statements. For the audit of the reliability of the accounts we have applied the attestation approach ever since our first opinion in 1994.

- We evaluate the accounting system to ensure it provides a good basis for producing reliable data.

- We verify key accounting procedures to ensure they function correctly.

- We make analytical checks of accounting data to ensure they are presented consistently and appear reasonable.

- We directly check a sample of accounting entries to ensure the underlying transactions exist and are accurately recorded.

- We check financial statements to ensure they present the financial situation fairly.

Regularity of transactions

Do the EU income and expensed payment transactions underlying the EU accounts comply with the rules?

The EU budget involves millions of payments to beneficiaries, both in the EU and in the rest of the world. The bulk of this spending is managed by Member States. To obtain the evidence we need, we assess the systems by which income and expensed payments (i.e. final payments and clearing of advances) are administered and checked, and we examine a sample of transactions.

Where the terms of the relevant international auditing standards have been met, we review and re-perform the checks and controls carried out by those responsible for implementing the EU budget. We thus take full account of any corrective measures taken on the basis of these checks.

- We assess the systems for revenue and expenditure to determine their effectiveness in making sure transactions are regular.

- We take statistical samples of transactions to provide a basis for detailed testing by our auditors. We examine the sampled transactions in detail, including at the premises of final recipients (e.g. farmers, research institutes or companies providing publicly procured works or services), to obtain evidence that each underlying event exists, is properly recorded and complies with the rules for making payments.

- We analyse errors and classify them as either quantifiable or not. Transactions are affected by quantifiable error if, based on the rules, the payment should not have been authorised. We extrapolate the quantifiable errors to obtain an estimated level of error for each area in which we make a specific assessment. We then compare the estimated level of error against a materiality threshold of 2 % and assess whether the errors are pervasive.

- Our opinions take account of these assessments and of other relevant information, such as annual activity reports and reports by other external auditors.

- We discuss all our findings both with the authorities in the Member States and with the Commission so as to confirm our facts are correct.

All our products are published on our website (eca.europa.eu). More information on the audit process for the statement of assurance can be found in Annex 1.1 to our 2018 annual report. Our website contains a glossary of the technical terms we use in our publications.

Contact

EUROPEAN COURT OF AUDITORS

12, rue Alcide De Gasperi

1615 Luxembourg

LUXEMBOURG

Tel. +352 4398-1

Enquiries: eca.europa.eu/en/Pages/ContactForm.aspx

Website: eca.europa.eu

Twitter: @EUAuditors

More information on the European Union is available on the internet (http://europa.eu).

Luxembourg: Publications Office of the European Union, 2019

| ISBN 978-92-847-2057-6 | doi:10.2865/642407 | QJ-03-19-425-EN-C | |

| ISBN 978-92-847-2007-1 | doi:10.2865/65338 | QJ-03-19-425-EN-N | |

| HTML | ISBN 978-92-847-2028-6 | doi:10.2865/70854 | QJ-03-19-425-EN-Q |

COPYRIGHT DISCLAIMER

© European Union, 2019.

Reproduction is authorised provided the source is acknowledged.

For any use or reproduction of the following pictures, permission must be sought directly from the copyright holders:

Page * (top right): © Shutterstock / science photo.

Page * (left): © Shutterstock / Sushaaa.

Page * © Shutterstock / Budimir Jevtic.

For the following pictures, reproduction is authorised provided the copyright holder, the source and the name of the photographers/architects (where indicated) are acknowledged:

Page * : © European Union 2018, source: European Court of Auditors.

Page * : © European Union, source: European Commission / Audiovisual Service.

Page * : © European Union, 2019, source: European Commission / Audiovisual Service, photographer: Etienne Ansotte.

Page * : © European Union, 2019; Europa building, architects: Philippe Samyn and Partners Architects & Engineers, Lead and Design Partner, Studio Valle Progettazioni Architects, Buro Happold Engineers.

Page * : © European Union, 2018, source: European Parliament, photographer: Mathieu Cugnot. Louise Weiss building, architects: Architecture-Studio.

Page * : (top left): © European Union, 2019, source: European Commission / Audiovisual Service, photographer: Jennifer Jacquemart.

Page * : (bottom): © European Union, 2018, source: European Commission / Audiovisual Service, photographer: Lukasz Kobus.

Page * : (left): © European Union, 2018, source: European Commission / Audiovisual Service, photographer: César Manso Arroyo.

Page * : (right): © European Union, 2015, photographer: Nikolay Doychinov.

Page * : (left): © European Union, 2018, source: European Commission / Audiovisual Service, photographer: Yorgos Karahalis.

Page * : (right): © European Union, 2018, source: European Commission / Audiovisual Service, photographer: Ezequiel Scagnetti.

Page * : (left): © European Union, 2019, source: European Commission / Audiovisual Service, photographer: Christian Jepsen.

Page * : (right): © European Union, 2010, source: European Commission / Audiovisual Service, photographer: Carlos Juan.

Page * : © European Union 2019, source: European Parliament, photographer: Ph. Buissin.

Page * : © European Union, 2018, source: European Commission / Audiovisual Service, photographer: Pierre Prakash.

Page * : © European Union 2019, source: European Court of Auditors.

Page * : © European Union, source: European Court of Auditors. Architects of the Court’s buildings: Jim Clemes

GETTING IN TOUCH WITH THE EU

In person

All over the European Union there are hundreds of Europe Direct Information Centres. You can find the address of the centre nearest you at: https://europa.eu/european-union/contact_en

On the phone or by e-mail

Europe Direct is a service that answers your questions about the European Union. You can contact this service

- by freephone: 00 800 6 7 8 9 10 11 (certain operators may charge for these calls),

- at the following standard number: +32 22999696 or

- by electronic mail via: https://europa.eu/european-union/contact_en

FINDING INFORMATION ABOUT THE EU

Online

Information about the European Union in all the official languages of the EU is available on the Europa website at: https://europa.eu/european-union/index_en

EU Publications

You can download or order free and priced EU publications from EU Bookshop at: https://op.europa.eu/en/web/general-publications/publications. Multiple copies of free publications may be obtained by contacting Europe Direct or your local information centre (see https://europa.eu/european-union/contact_en)

EU law and related documents

For access to legal information from the EU, including all EU law since 1951 in all the official language versions, go to EUR-Lex at: http://eur-lex.europa.eu/homepage.html?locale=en

Open data from the EU

The EU Open Data Portal (http://data.europa.eu/euodp/en/data) provides access to datasets from the EU. Data can be downloaded and reused for free, both for commercial and non-commercial purposes.