Executive summary

The European non-life insurance market experienced a year-over-year (YoY) growth in premiums in 2016, with the majority of premiums generated by the “medical expenses insurance”, “fire and other damage to property insurance” and motor insurance lines of business. Life insurance premiums decreased in a majority of Member States, and there was an increase in “hybrid life insurance products” and new “with-profit life insurance products”, where the economic value of embedded guarantees appears significantly lower compared to traditional with profit products.

Digital technologies continue to progressively penetrate the European insurance sector; leveraging their cutting-edge data analysis tools and technologies, InsurTech start-ups have proliferated, frequently specialising in developing specific areas of the insurance value chain. Distribution channels have been most targeted to date. Peer-to-peer insurers often follow this pattern, though their business model may not in all cases be very different from that of traditional undertakings, as they can only operate in the EU through a licensed insurance undertaking or through a broker/intermediary in cooperation with a licensed insurance undertaking.

The still moderate use of telematics devices in health, motor or household insurance has enabled the development of usage-based insurance (UBI) products adapted to the characteristics and behaviour of consumers. These can also enable improved customer relationships or the prevention of risks, although, linked to the broader Big Data phenomenon, UBI could also have an impact on the access to insurance of high-risk consumers. The use of other technical innovations, such as blockchain technology or artificial intelligence, still appears limited in insurance, although there are some examples where they are already being applied in practice.

It is increasingly evident that digital technologies represent a key competitive factor and a source of economic growth; in this context some national competent authorities (NCAs) have been actively promoting financial innovation through a series of initiatives, such as Innovation Hubs, regulatory sandboxes, or public-private partnerships like start-up accelerators. Other than in the area of financial innovation, in 2016 NCA’s consumer protection activities predominantly focused on supervising unit-linked life insurance products and product information issues.

From a consumer protection perspective, it is also noteworthy that consumer complaints in the insurance sector considerably increased in 2016. This increase has taken place in most Member States and has been particularly significant in the non-life insurance sector, which to a limited extent could be related to the stronger market growth explained above. Moreover a significant part of these complaints are related to claims handling issues. In this regard, the claims ratios (i.e. the proportion of premiums used to pay claims) in lines of business such as “legal expenses insurance”, “assistance”, or “miscellaneous financial loss” are below 50%, and in these lines of business high commission rates can be seen compared to other lines of business. However in 2016 the claims acceptance rates of the last two lines of business were relatively high compared to legal expenses insurance.

As far as the pensions sector is concerned, taking into account the inherent specificities of the pensions market and bearing in mind that the delineation between pension pillars in some Member States can be complex, most of the Member States that provided data to EIOPA experienced a YoY increase in the number of active members both in the personal and occupational pensions sectors. This is likely related to the moderate recovery of the European economy and labour markets, as well as the reforms introduced by some Member States in recent years.

Life-cycle funds are a relatively new approach to retirement investment in several European pension markets. These appear to quickly gain momentum in some markets, reflecting once again changes to national pension legislation. This interest in life-cycling is also reflected in the pan-European personal pension product (PEPP) legislative proposal.

The use of digital technologies such as mobile phone applications or robo-advisors in the pensions sector is still moderate. This partly could be due to legacy issues such as Defined Benefit (DB) schemes, where the outcome is pre-determined in advance and there is little need for engagement from the individual. However the shift from DB to Defined Contribution (DC) observed in several Member States together with other developments such as the increasing penetration of smart phones and digital technologies in the European economy are progressively changing this situation.

Finally, the number of complaints in the pensions sector slightly increased in 2016, although in several Member States the increase is too low to draw conclusions for the whole sector based on them. During 2016 one of the main priorities of NCA’s consumer protection activities in the pensions sector was to ensure that individuals were provided with adequate and transparent information about their pensions rights and expected retirement income.

Looking ahead, it is notably that 2018 and 2019 will bring significant improvements and changes in the EU regulatory environment related to insurance and pensions.(1) These can be expected to impact trends of all types in the future, though the impacts may take a number of years to become clear.

(1) The application of the Insurance Distribution Directive and the Packaged retail investment and insurance-based products (PRIIPs) Regulation will resume in 2018, and the Institutions for Occupational Retirement Provision Directive (IORP II) in January 2019.

Introduction

Article 9 of EIOPA’s founding Regulation requires the Authority to “collect, analyse and report on consumer trends.”(2) The term consumer trend is not defined in the EIOPA Regulation. EIOPA has devised the following working definition: “Evolutions in consumer behaviour in the insurance and pensions markets related to the relationship between consumers and undertakings (including intermediaries) that are significant in their impact or novelty”.

To date, EIOPA has published five Consumer Trends reports. The report covers trends both in the insurance sector and in the pensions sector. A description of the main market developments is provided in the first section, complemented with the analysis of quantitative data extracted from EIOPA’s Solvency II database. Then, a series of financial innovations are subsequently analysed. EIOPA decided to place special focus on financial innovations as a distinctive feature of this year’s report, in response to the increasingly prominent role played by digital technologies.

Next, and bearing in mind the supervisory background of this report, an analysis of last year’s consumer complaints and NCA consumer protection activities is provided. One of the key objectives of the report is to try to identify risks for consumers arising from trends in the market, which may require specific policy proposals or supervisory action from EIOPA and/or its Members. Moreover, by highlighting the non-confidential activities reported by NCAs for their respective jurisdictions, EIOPA contributes to the task that it has been assigned by its founding Regulation of encouraging a common supervisory culture amongst its Members through the promotion of exchanges of information between competent authorities.(3)

Not all trends identified exist in all the EU Member States; in some Member States the trends described may not exist, in others they may only be at a very incipient stage, while in other Member States the trends might be already consolidated for a number of years. However, the fact that one Member State is not mentioned under a specific trend does not necessarily mean that such a trend does not exist in that Member State or that the relevant NCA has not undertaken any activities in that specific field.

In order to meet the above objectives, EIOPA has developed a Methodology (4) for producing a Consumer Trends Report on an annual basis (see Annex I for further details). It essentially consists in the collection of quantitative and qualitative consumer information from EIOPA’s Members as well as from stakeholders. This year’s report also includes interviews of stakeholders providing their first hand views on key developments that are taking place in the markets.

There are certain limitations to the methodology, for example, a number of NCAs were not in a position to provide all the input requested by EIOPA and that given that it is only the first year of the new Solvency II reporting framework its data must be interpreted cautiously. However the information gathered is extensive, both of quantitative and qualitative nature, and from a wide variety of sources, which allows EIOPA to confidently identify consumer trends in the European insurance and pension markets.

(2) Article 9(1)(a), Regulation 1094/2010 establishing EIOPA, http://eur-lex.europa.eu/LexUriServ/LexUriServ.do?uri=OJ:L:2010:331:0048:0083:EN:PDF

(3) Article 29 of EIOPA Regulation

(4) EIOPA, Consumer Trends Methodology, November 2012, https://eiopa.europa.eu/Publications/Reports/2012-11_Methodology_on_collecting_consumer_trends.pdf

Insurance sector

1. Market growth

1.1 Life insurance

In a context of a persistent low interest rate environment and moderate economic growth, coupled with the introduction of the Solvency II regulatory framework, life insurance premiums decreased in a majority of Member States during 2016.

Guaranteed products, such as with-profit life insurance, put considerable pressure on insurance undertaking’s liabilities in the context of a low interest rate environment, prompting business shifts. As a result, based on the information provided to EIOPA by NCAs, with-profit life insurance premiums have decreased in several Member States including Croatia (-10.8%), Sweden (-6%), Latvia (-13.5%) or Portugal (-38.4%). However, with-profit premiums have also increased in Member States such as Estonia (+7.1%), Luxembourg (+2.4%) or Norway (+1.9%). Indeed in some Member States with profit products are still attractive for consumers since the guarantees offered may exceed those of comparable banking products.

While indeed the trend in several Member States is to progressively introduce products with lower guarantees, until existing long-term contracts mature, with-profits policies remain the largest single life insurance line of business in terms of GWP, as it can be observed in figure 2.

Source: Swiss Re Institute, Sigma Explorer (5)

Source: EIOPA Solvency II database

Source: EIOPA Solvency II database

In 2016 unit-linked and index linked life insurance was the second most important life insurance line of business with over 239 billion GWP. While unit-linked life insurance premiums grew in Member States such as Bulgaria (+115.9%), France (+16.9%) or Norway (+20.3%) a majority of Member States reported a year-on-year drop of unit-linked life insurance premiums including Malta (-30.7%), Italy (- 24.5%), Slovakia (-11%) or the Netherlands (-4.9%).

In Finland the decrease in unit-linked life insurance premiums was motivated by a series of factors such as fluctuations in the stock market, discussions on the taxation regime of insurance products, or the strategic decisions of some large financial conglomerates. In Poland (-21.3%) poor performance in recent years together with some mis-selling scandals have resulted in a major drop of unit-linked premiums in 2016.

During 2016, most of the new life insurance contracts (that is by number of contracts) were in the “other life insurance” line of business, which generally covers premiums from products such as traditional life insurance protection products without an investment component or mortgage protection life cover (term insurance), and which are often sold through banking institutions.

While the number of new “other life insurance”6 contracts as well as the commissions paid for the sale of these contracts (see figure 7 below) are more than double than for the other life insurance lines of business, in terms of GWP this line of business is still relatively small as shown in figure 2 above. Member States that experienced a premium growth in this line of business include Malta (+19.7), Italy (+4.2%), Hungary (+42.6%), Spain (+32%) or Slovenia (+5.4%).

Finally, it is remarkable the fact that the number of new with-profit life insurance contracts was greater than the number of unit-linked and index linked contracts in 2016, which shows that consumers still look for some level (even if small) degree of guarantee when purchasing life insurance products.

(5) http://www.sigma-explorer.com/explorer/map/index_map.php?indis=rpgr&modi=life|®i=WOR&ext=1

(6) Does not include the new contracts data from ES.

1.2. Non - Life insurance

Most Member States experienced a YoY premium increase in their respective non-life insurance markets. As it can be observed in the figure below, the premium growth has generally been stronger in Eastern European Member States, while in Central and Northern Europe the premium growth has been more moderate.

According to the information provided to EIOPA by NCAs, the increasing sales of motor vehicles are reportedly one of the key drivers of the motor insurance premium growth experienced in Member States such as Portugal (+3.5%), Bulgaria (+5.5%), France (+2.2%) or Slovakia (6.7%). In other Member States such as Lithuania (+16.2%), UK or Poland (108.7%), the GWP growth in the motor insurance sector was motivated by higher premiums. In Italy (-3.1%) motor insurance premiums decreased as a result of increasing competition and reduced claims costs, in part owing to the increasing penetration of telematics-based motor insurance policies.

The sum of the lines of business “motor vehicle liability insurance” and “other motor insurance” accounted for over 124 billion euros in 2016. This can be observed in the figure 5, which captures the GWP from both retail and corporate clients.

The line of business “medical expenses insurance” was the biggest individual non-life insurance line of business in 2016, although “workers compensation insurance” and “income protection insurance” are also health-related (accident) lines of business. This is also the case for the life insurance line of business “health insurance” which covers invalidity and critical sickness policies underwritten by life insurance firms.

Accident and health insurance GWP increased in Member States such as Malta (+58.5), Luxembourg (+13.2%), France (+13.5%) or Croatia (+10.4%). In Lithuania (+15.5%) employers are increasingly offering health insurance coverage to their employees to make their salary packages more attractive. In the UK the launch of Flood Re has given over 50.000 customers in flood-prone areas access to flood cover.

The line of business “Fire and other damage to property” generated over 98 billion euros in 2016. Household insurance GWP increased in a majority of Member States during 2016, including Austria (+2.4%), Estonia (+10.3%) or Lichtenstein. In Romania the growth in the household insurance market is linked to the increase in the number of mortgage loans, which commonly are given together with insurance policies such as household insurance.

Source: Swiss Re Institute, Sigma Explorer

Source: EIOPA Solvency II database

In 2016, the claims ratio (7) for the “Fire and other damage to property” line of business was 51%, which means that half of the premiums were used to pay claims. The claims ratios for other non-life insurance lines of business are shown in the figure 6.

The fact that claims ratios for “medical expenses insurance” and “workers compensation insurance” are 84% and 87% respectively suggests that they are good value for money for consumers and that they may be relatively expensive for insurance undertakings, (8) possibly as a result of increased health care costs, although cross-selling with other less expensive lines of business (e.g. legal expenses insurance) might mitigate costs.

Source: EIOPA Solvency II database

The claims ratios for lines of business such as assistance (e.g. assistance to motor vehicles on the road or travel insurance) or miscellaneous financial loss (e.g. employment risks in payment protection insurance, mobile phone insurance or cyber insurance) are the lowest. However the claims acceptance rates are very high (see figure 13 below), which suggests that consumers buy them for peace of mind while they are away from home but in the end they rarely need to use them or that they are not fully aware of the coverage that they have.

It the UK single trip single-trip travel insurance policies have fallen by 76% in the past decade, although multi-trip travel insurance policies sold via packaged bank accounts or credit cards have increased. Another relevant development impacting the travel insurance market is increasing risks in several popular tourist destinations; for example in the Italian travel insurance market (+7%), some travel insurance policies have started to offer trip cancellation coverage in case of terrorist attack.

(7) Claims incurred in the reporting period as defined in directive 91/674/EEC where applicable: the claims incurred means the sum of the claims paid and the change in the provision for claims during the financial year related to insurance contracts. This shall exclude claims management expenses.

(8) For further information see the Net Combined Ratio across business lines on page 31 of the EIOPA June 2017 Financial Stability report: https://eiopa.europa.eu/Publications/Reports/2.The%20European%20insurance%20sector_FSR-June-2017.pdf

Finally, the commission rates for the lines of business “miscellaneous financial loss” and “legal expenses insurance” are the highest amongst the life and non-life insurance lines of business, as represented in figure 7.

Source: EIOPA Solvency II database

The percentage of the premiums paid in commission for life insurance lines of business are lower than for non-life insurance lines of business, with the exception of “other life insurance”. From a consumer protection perspective, high commission rates could provide incentives to distribution channels to sell products to consumers so as to generate commissions, potentially triggering a conflict of interests that may not be effectively mitigated, which would lead to poor consumer outcomes. However commission rates need to be jointly analysed with other retail risk indicators, and certainly they may also not lead to consumer detriment, especially when there are adequate governance and control frameworks in place to mitigate potential conflicts of interest.

2. Financial innovation

As announced in the introduction, this year’s Consumer Trends report places an increasing focus on financial innovation in view of the increasing penetration of digital technologies in the insurance and pensions sectors. In view of the findings of previous reports, a number of topics were selected to be analysed in the present report: InsurTech firms / start-ups, new life insurance policies, the use of telematics in insurance, peer-to-peer insurance and supervisory activities to foster financial innovation.

Certainly, there are many more innovative developments which deserve to be carefully analysed. Last year’s report for instance analysed the use of geolocation technology in household insurance or mobile phone applications in insurance. Other developments such as block-chain, artificial intelligence or the application of precision medicine in insurance could certainly be topics to be more thoroughly analysed in forthcoming reports.

2.1. InsurTech firms/start-ups

Compared to other sectors, the insurance sector has been relatively slow to embrace new technologies, but there are signs that this situation is rapidly changing. Many existing insurers (so-called ‘incumbents’) are reportedly embarking on ambitious digital transformation projects, and upgrading their digital capabilities through the set-up of in-house and external innovation labs, partnering with large tech firms and/or collaborating with InsurTech start-ups.

By cooperating with InsurTech start-ups, incumbents can benefit from their cutting-edge data analysis tools and technology. InsurTech start-ups offer their technological expertise to incumbents all along the insurance value chain: use of big data and open data for pricing and profiling customers, development of robots and connected objects, development of new distribution channels that rely more on mobile solutions such as the increasingly popular chat boxes etc.

Start-ups also benefit from such collaboration,namely through access to incumbents’ large customer databases or underwriting and regulatory expertise. The latter is particularly relevant in insurance given the comprehensive regulatory framework under which insurance is conducted, and this is also the reason why a number of NCAs have set up Innovation Hubs to help start-ups navigate the applicable regulations (see figure 8).

Source: EIOPA InsurTech Roundtable, presentation by Finleap (9)

If InsurTech start-ups decided to enter the insurance market alone, they can only be registered under one of two distinct categories: as an insurance undertaking or an insurance intermediary. Regulators typically consider that similar risks should be regulated in similar ways, and as such, new entrants should be regulated like any other insurance firm in so far as the risks are similar. However the Solvency II Directive also explicitly states that its rules need to be applied proportionally to the nature, scale, and complexity of the risks inherent in the business, in particular to small insurance undertakings.(10)

Moreover, as a result of new technologies and actors (e.g. InsurTech start-ups or IT companies), which often specialise on specific areas of the value chain, there can be increased fragmentation of the insurance value chain; this possible scenario raises a number of challenges from a supervisory standpoint. Indeed it can bring complexity and make overall risks harder to capture, although it can also increase resilience and reduce the impacts of individual failures. It is therefore necessary to assess how existing legislation such as Solvency II’s requirements on the supervision of outsourced functions and activities will apply in view of the impact of financial innovation.(11)

2.2. New life insurance products

In the on-going context of low interest rates environment and the increasing aging population, guaranteed products have continued to give way to non or less guaranteed products; insurance products in which insurance undertakings guarantee an annual benefit and thereby bear the risk of adverse financial markets are progressively being replaced by products in which customers increasingly bear to a greater extent the investment risk themselves.

This trend is driven by commercial strategies put in place by insurance undertakings towards the selling of unit-linked products and/or to incentivise consumers to switch from guaranteed products to products with fewer guarantees. As a result pure unit-linked life insurance products, where there are no financial guarantees at all and the investment risk is born completely by the consumer, are increasingly popular in some Member States. However in other Member States, there is evidence that poor investment performance in recent years has led consumers to demand again more traditional life insurance products.

Insurance companies also increasingly offer new “with profit life insurance” products, where the economic value of embedded guarantees and the associated interest rate risk is significantly lower compared to traditional with profit products. Some of the main features of these new life insurance products are the following:

- The full guaranteed interest rate is not guaranteed for each single year, but only for a certain number of years or on average for the whole life time of the contract.

- Very often no interest rate is explicitly guaranteed, but insurers guarantee that the accumulated capital at least reaches the sum of paid premiums at the end of the contract or until the start of annuity payments (minus fees and charges and without taking into account inflation).

- For annuity products the conversion rate which is used to convert the accumulated capital into an annuity is set at the time when annuity payments start. Only a very small conversion rate is already guaranteed at the inception of the contract.

Another example of new life insurance products are the hybrid products that are a combination of pure unit-linked products and traditional with-profit products. The accumulated capital of such contracts is typically split into a unit-linked part and a traditional mathematical reserve calculated with a guaranteed interest rate. These types of products may sometimes include sophisticated financial strategies and automatic or discretionary switching mechanisms from one component to the other one.

Moreover new investment strategies are being developed and marketed to consumers, with non-guaranteed products typically including a higher proportion of investments in equities and fewer investments in bonds relative to total investment assets. The underlying assets are also frequently invested either in mutual funds or internal funds managed by the insurers themselves. Similarly, the proportion of alternative investment products, e.g. in infrastructure, forestry and alternative credit, is generally larger in non-guaranteed products. Finally, in some Member States it has also been observed a trend towards the inclusion of biometric risks coverage such as death, disability, critical illness and sometimes health in life insurance products.

From insurance undertakings’ perspective, life insurance products with low or no guarantees offer the advantage of reducing the insurer’s liability resulting from contractual guarantees. From the consumers’ point of view, some consumers, especially those with a higher risk appetite, might prefer a product with low guarantees since such products frequently offer more investment choices as well as the chance of a better return in exchange of a higher risk.

However, since a major drop in the stock market may lead to a significant reduction in the customer’s savings in unit-linked life insurance products, contrary to the downside protection offered by a traditional contract, there is the danger that customers who do not have the adequate financial capabilities to understand the risks end up buying products that carry more risk than they wished to take on. This can be exacerbated by the complexity of some of the investment options offered. Situations of unmitigated conflicts of interest which led to poor outcomes for consumers have also been reported in a number of Member States in recent years, although the new governance requirements introduced by the IDD are expected to mitigate some of these risks.

(9) EIOPA InsurTech Roundtable, April 2017, [Link]

(10) Article 29 Solvency II Directive

(11) Article 38 Solvency II Directive

2.3. The use of telematics in insurance

The Internet of Things (IoT), i.e. the interconnection via the Internet of devices such as mobile phones, connected cars, health wearable devices or smart homes, is becoming a prominent part of our daily lives. Many businesses, including insurance undertakings, are therefore trying to determine how these developments can be used in their day-to-day activities as well as to create deeper relationships with their customers.

In insurance, the use of telematics is commonly associated with usage-based insurance (UBI), i.e. insurance products measuring consumer’s behaviour and environment to perform risk assessments and price discount rewards. For example, in motor insurance the use of telematics (via a black box installed in the car, or an app in the mobile phone) can track the number of kilometres driven, the average speed, acceleration, geolocation etc. and price insurance policies with this information.

Source: Institute of International Finance. Innovation in Technology: How technology is changing the industry; Institute of International Finance; September 2016 https://www.iif.com/system/files/32370132_insurance_innovation_report_2016.pdf

In wearable devices tracking variations in blood pressure, glucose levels, number of steps walked, calories consumption, places visited etc. can also be used to perform risk assessments and price health or life insurance. This is also the case with the information provided by smoke, flood, energy consumption or security sensors installed in smart homes.

However telematics are much more than only UBI. The data collected by telematics devices can be used to personalise products and services, improve the client’s user experience (“UX”) and increase their level of engagement. For example telematics can be used to provide road assistance services, theft notifications, stolen vehicle recovery, warning of potentially dangerous driving behaviours, real time coaching, raise awareness of possible health risks, provide incentives to drive safer etc. Telematics devices may also help expedite claims handling and reduce fraud by providing accurate information about the accident dynamics (e.g. geolocation and speed).

Motor insurance is the line of business that has seen a greater penetration of telematics to date, having a strong presence in Italy (circa 19% of total MTPL policies in 2016) followed by the UK. As cars become increasingly connected with more powerful navigation systems and new sensors embedded into them, the penetration of policies based on the time spent driving — “pay as you drive” policies — or adapted to the driving habits — “pay how you drive” policies are also expected to increase.(12)

UBI products could also come with some dangers that regulators have to be aware of and closely monitor. Linked to the Big Data phenomenon (greater availability and capacity to process data which is not only comprised of telematics data), more detailed information about risk may involve “anti-selection” - in competitive markets high-risk groups could suffer as they do not get any coverage at all anymore or it becomes extremely expensive. This can be particularly sensitive from an “ethical” / fair treatment perspective where information is being used to price risks that do not reflect the behaviour or choices of the individual, or in the case of compulsory insurance.

In contrast, other segments of the population could face better access conditions; young inexperienced drivers installing telematics devices in their vehicles reportedly often pay lower premiums.(13) Moreover other risks that could arise from telematics for consumers include the reduced comparability of (individualised) policies and prices, or also privacy-related issues such consumer’s consent and awareness of the use of their personal data.

(12) Deloitte surveyed around 15,000 customers from Austria, Belgium, France, Germany, Ireland, Italy, Poland, the Netherlands, Spain, Switzerland and the United Kingdom. Based on that survey, Deloitte estimates that by 2020 the market share for UBI products in motor insurance issued in these eleven countries could reach 17 per cent which represents a market in excess of €15bn. https://www2.deloitte.com/content/dam/Deloitte/be/Documents/finance/European-Motor-Insurance-Study_2nd-edition_November-2016.pdf

(13) According to a study published by the British insurance intermediary association BIBA, the accident rate for young drivers installing telematics devices in their car reduces from 1 in 5 drivers to 1 in 16: https://www.biba.org.uk/press-releases/biba-research-reveals-750000-live-telematics-based-policies/

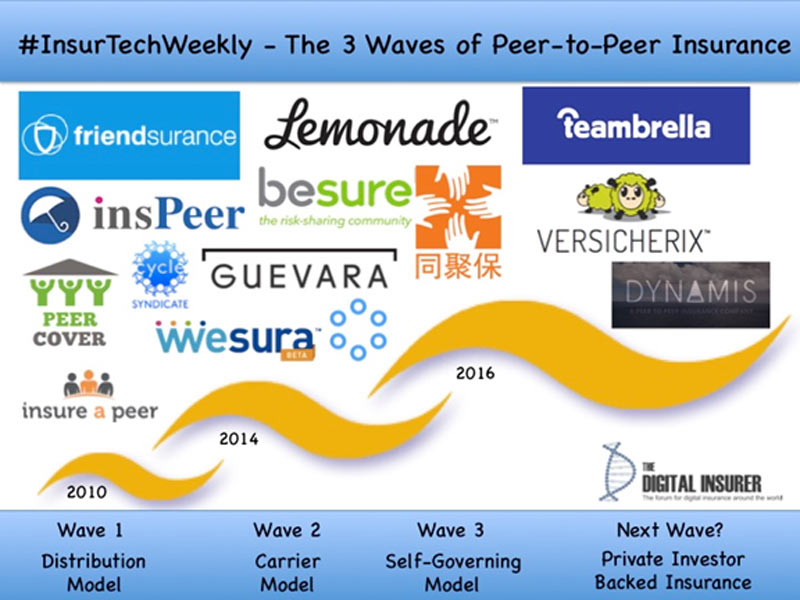

2.4. Peer-to-peer insurance

The Czech Republic, France, Germany, Italy, Norway, the Netherlands, and the UK have seen the recent emergence in their respective jurisdictions of so-called peer-to-peer (P2P) insurance models. While their differences from traditional undertakings such as mutual insurers is not always evident (some consider them as “micro-mutual insurance”), in essence P2P is generally commercialised as a risk sharing network where a group of individuals with mutual interests or similar risk profiles pool their “premiums” together to insure against a risk. The size of the group depends on the type of insurance and the expected benefits to be generated.

P2P insurance firms group together consumers with similar specialised insurance needs and obtain an attractive price/product for them by pooling their funds together and using the power of collective bargaining. Moreover, P2P insurance models also try to foster lower-risk, responsible behaviours amongst the members of the group through transparency, social emulation and economic incentives.

Indeed P2P insurance firms typically redistribute surplus funds amongst the members of the pool at the end of the year. They also promote transparency in its operations by pooling premium funds with groups of acquaintances; members usually know who is in the group, who is filing a claim, and how much money is in the pool.

By pooling together small groups of people with mutual interests and redistributing amongst them the non-used funds at the end of the year, P2P insurance aims to mitigate the conflict / moral hazard that could potentially arise between a traditional insurer and a policyholder when an insurer keeps the premiums that it doesn’t pay out in claims.

In most peer-to-peer models premiums from the members of the pool are collected in advance in order to create an ex-ante protection pool. However there are also some P2P models where funds are called only after the claim occurs. Moreover, depending on the level of intermediation, there are also different types of P2P insurance models, as can be observed in figure 10.

Source: The Digital Insurer(14)

In Europe, P2P insurance can only be provided either directly through a licensed insurance undertaking or through a broker/intermediary in cooperation with a licensed insurance undertaking (i.e. the first two “waves” in the graphic above). Currently peer-to-peer insurance in Europe cannot operate as a decentralised two-sided platform like other peer-to-peer models in other sectors of the economy.(15)

During the EIOPA InsurTech Roundtable held in April 2017, some participants suggested that regulatory authorities should assess the adequacy of the current insurance rules in relation to the legal status of a peer group of individuals or the “money pool” created from the contributions of a group of individuals. The definition of ‘insurance’ was also discussed; is P2P insurance – i.e. the constitution by a peer group of a “money pool”, dedicated to paying their claims up to its original amount – really insurance? Some participants suggested that there was a case for developing specific regulation for P2P insurance.(16)

(14) Introducing the third wave of peer-to-peer insurance, the Digital Insurer, https://www.the-digital-insurer.com/blog/insurtech-teambrella-and-the-third-wave-of-peer-to-peer-insurance/

(15) For example digital platforms that have recently been created in the apartment rentals business.

2.5. Other financial innovations

The topic of distributed ledger technology / blockchain has attracted a lot of attention in the specialised media but there are still very few examples of its practical use in insurance. One of this few examples is the new travel delay and cancellation policy “fizzy” started to be marketed by AXA in 2017, which offers automatic compensation to policyholders whose flights are delayed with the use of the Ethereum blockchain.(17)

With some few exceptions, the use of blockchain in insurance is still at an experimental phase; some major insurance players have group up together in the B3i initiative to explore the potential use of distributed ledger technology in the insurance sector. The French insurance industry association FFA is also working on a “proof of concept” with its members. Moreover, the UK NCA is also investigating this new technology and has published a discussion paper on this topic where it analyses possible use cases of blockchain in areas such as the reinsurance markets, regulatory reporting, recordkeeping and auditability or the mitigation of financial crime.(18)

Also with the objective of reducing operational costs, Danish insurers are reportedly shifting towards implementing automated claims handling systems for minor claims such as windshield damages, where payments are transferred automatically, without ever being checked by a claims clerk. Also in Norway, insurers are reportedly working towards automating the claims handling process in a large proportion of damages so that they are settled or concluded within an hour. Artificial intelligence technology is also reportedly being used by Zurich insurance or the start-up Lemonade to process personal injury claims.(19)

Moreover, in respond to insurer’s desire to assess risk more accurately and rate accordingly the use of geo-location technology in the provision of flood cover, complementing the information traditionally provide by postcodes, is more and more common in Member States such as Ireland and Spain.(20) In the former Member State insurers are progressively moving towards paperless processes, which have evolved from just emailing documents to providing a platform where all the consumer’s insurance documents are stored electronically and accessible to consumers online.

In Malta and the Netherlands it has also been reported an increasing interest of market participants on robo-advisors. An increasing demand for cyber insurance policies has also been reported in the German and Slovak markets. Also in Slovakia, some life and health insurance products now offer the service “Diagnose.me”, which allows consumers to get a second medical opinion online.

The use of QR codes in the Czech Republic and Poland to facilitate payments is another example of the use of the increasing use of digital technologies in insurance. In the case of Poland, the QR Code with information about the vehicle and the vehicle owner is incorporated directly into the vehicle registration card. The Czech and Slovak markets have also recently starting using biometric signatures as an acceptable alternative to the traditional “paper” signature.

In Portugal and Romania, motor insurance is reportedly being sold through machines similar to ATMs known as “payment kiosk” or “payment points”, which, as any other distribution channel, shall comply with the applicable insurance distribution legislation. This is also the case of comparison websites, which are also reportedly increasing in Portugal. The German insurance intermediaries association BVK recently won a court case against a popular comparison website in Germany.

In the life insurance sector, in Member States such as Sweden insurance undertakings are increasingly taking into consideration environmental and sustainability aspects in their long-term investments. Also in the area of investments, Danish insurance undertakings increasingly invest in alternative asset classes such as private equity, infrastructure, forests or hedge funds. In Finland, life insurance undertakings are actively cooperating with health care companies and health and wellbeing device and service providers including InsurTech start-ups.

Finally, the development of precision medicine, i.e. the customization of healthcare according to the genetic and epigenetic characteristics of individuals, which includes analysis of lifestyle and environment, could potentially have a considerable impact on the health and life insurance sector in the future; it would allow the possibility to perform more accurate risks assessment, which on the one hand could enable improved medical treatments, but on the other hand it could have access / exclusion implications for high-risk consumers.

The use of genetics data in insurance is allowed in several Member States under certain circumstances (e.g. explicit consent of the policyholder, or the consumer having done genetic tests himself and is obliged to reveal the results or the insurance contract is above certain financial thresholds). It should also be noted that some Member States have signed and ratified the International Convention of Human Rights and Biomedicine which restricts the use of predictive genetic tests.(21) Moreover it should also be noted that nowadays consumers could potentially make insurance choices themselves in view of such data to the disadvantage of insurance undertakings.

(17) AXA goes blockchain with fizzy, September 2017, https://www.axa.com/en/newsroom/news/axa-goes-blockchain-with-fizzy

(18) Discussion Paper on distributed ledger technology, UK Financial Conduct Authority, April 2017, https://www.fca.org.uk/publication/discussion/dp17-03.pdf

(19) Zurich Insurance starts using robots to decide personal injury claims, Reuters, 18 May 2017, https://www.reuters.com/article/zurich-ins-group-claims/zurich-insurance-starts-using-robots-to-decide-personal-injury-claims-idUSL2N1IK268

(20) Further information about the use of geo-location in insurance please consult pages 27 and 28 of last year’s EIOPA Fifth Consumer Trends report: https://eiopa.europa.eu/Publications/Reports/06.0._EIOPA-BoS-16-239%20-%20EIOPA%20Fifth%20Consumer%20Trends%20report%20-%20Clean%20after%20BoS.pdf

(21) Convention for the protection of Human Rights and Dignity of the Human Being with regard to the Application of Biology and Medicine: Convention on Human Rights and Biomedicine, http://www.coe.int/en/web/conventions/full-list/-/conventions/treaty/164/signatures?p_auth=3AeWcIJF

2.6. NCA initiatives to foster financial innovation

As described above these lines, digitalisation in the insurance sector is rapidly accelerating. This has triggered a strong focus on this area not only amongst stakeholders but also amongst several NCAs. Indeed, as the nature of insurance business changes due to technological innovation, regulators also need to adapt their resources and activities to these developments.

In addition to exploring the benefits and risks arising from financial innovations and ways to address them, some regulators also have sought to foster innovation. It is argued that in an increasingly globalised and digital economy, innovation is a key competitive factor. Various initiatives have thereby arisen, guided by supervisors’ overarching roles for safeguarding financial stability and protecting consumers. Key supervisory principles such as technological neutrality, proportionality, market integrity and consistency from an activity-based and channel-based perspective shall also be respected at all times.

To date so-called Innovation Hubs (also referred to as InsurTech portals or InsurTech Laboratories) have been the most widespread initiative across Member States, including Austria, Belgium, Denmark, Finland, Norway, Lichtenstein, Lithuania, the Netherlands and the UK. The approach essentially consists of a single point of contact for InsurTech-related issues, where financial regulators typically offer bespoke assistance to firms not accustomed to dealing with financial regulations and/or which have doubts about how certain financial regulations would apply to their activities.

The NCAs of the UK and the Netherlands also have established what is known as regulatory sandboxes. Such a sandbox is comprised of a set of rules that allows innovators to test their products/business models in a live environment without following some or all legal requirements, subject to predefined restrictions which are applied proportionally (e.g. limitations on number of clients, risk exposure; time-limited testing; set of predefined exemptions; testing under regulator’s supervision). If, after sandbox testing, the firm wants to offer its services to the wider market, it shall comply with existing regulatory frameworks applicable to that type of activity.

Finally some Member States are exploring the option of public-private partnerships to foster financial innovation in their financial markets. For instance this is the case in Belgium, where the Belgian government is supporting the B-Hive (22) start-up accelerator where incumbents and start-ups exchange resources, know-how and experiences and cooperate in the funding and development of innovative solutions.

In order to support the increasing focus on financial innovation activities, NCAs are equipping themselves with dedicated FinTech / InsurTech Task Forces for gathering knowledge and expertise across the different teams within the Authority. The NCAs of France, Germany, Italy, Iceland, Ireland, Romania and Poland are examples of NCAs which have set up such FinTech/ InsurTech-dedicated teams. EIOPA has also recently created its own InsurTech Task Force, which will be responsible for the upcoming work of the Authority in areas such as Big Data or cyber risk.

More broadly, some NCAs are accompanying the above initiatives with a comprehensive communication strategy aiming to promote their respective jurisdictions as an attractive hub for financial innovation. (23) Other authorities have reached cooperation agreements with 3rd country supervisory authorities to exchange information on emerging innovation trends, potential joint innovation projects, and regulatory issues pertaining to innovative financial services.(24) Finally, some authorities have also recently established Fintech stakeholder groups,(25) and others are actively sharing their views in InsurTech conferences and publications as means of promoting reflection and discussion about the topic.

3. Consumer complaints

The methodology of the Consumer Trends report includes the collection of aggregated complaints data on an annual basis. The analysis of consumer complaints can help identify possible consumer protection issues arising in the market, and vice-versa.

In 2016 the number of consumer complaints in the insurance sector has considerably increased (+31%) compared to the previous year, as it can be observed in the following figure:

Source: EIOPA Committee on Consumer Protection and Financial Innovation

It is important to note that the graphic above includes complaints that are upheld (justified) as well as those which may not be substantiated. It could also be the case that some consumers unsatisfied with their insurance policy do not formally lodge a complaint. Many consumers only lodge a complaint in the case the insured event manifest and do not receive a satisfactory response to their claim. It can also be useful to put into perspective the number of complaints with the number of contracts; based on the data from 15 Member States, (27) in 2016 there were roughly 3 complaints per 1000 insurance contracts (1 complaint per 1000 contracts in 2015).

(22) https://b-hive.eu/brussels

(23) For example, the Netherlands has appointed a “Fintech Ambassador”, and the UK a “Special Envoy for FinTech”. Other Authorities have organised events on the topic such as the Monetary Authority of Singapore’s 2016 “Fintech Festival” [Link].

(24) For example, the joint agreement reached between ACPR and the Monetary Authority of Singapore on 27 March 2017 [Link].

(25) For example, Bafin’s Fintech Council created on 22 March 2017 [Link].

(26) Does not include complaints data from CY, FI and NL. In the case of FI insurance undertakings have been developing their record keeping of complaints and the data is not comparable from year to year.

(27) Data from BG, HR, CZ, HU, IS, IE, LV, LI, LT, MT, NO, PL, PT, RO and SI. These are the Member States that provided data to EIOPA both on complaints and on number of contracts for 2015 and 2016

Source: EIOPA Committee on Consumer Protection and Financial Innovation

Source: EIOPA Solvency II Database

Based on the data provided to EIOPA, the increase in the total number of complaints has been strong both regarding life and non-life insurance products. However, while most of the Member States experienced an increase in the number of non-life insurance complaints(28), life insurance complaints declined in almost as many MSs as in those were they increased;(29) the high upsurge in the number of life insurance complaints was mainly triggered by strong increases experienced in a small number of Member States.

With the exception of PPI, all of the non-life insurance product categories experienced a year-on-year increase in the number of complaints. The increase for the “other non-life insurance” category was particularly significant, both in total number of complaints and in number of Members States. This product category includes a wide array of products (depending on the Member State) such as legal expenses insurance, mobile phone insurance, extended warranties, professional indemnity insurance, third party liability insurance, sea vessels liability etc.

Some of the products included in the non-life insurance product category are often sold through cross-selling practices, i.e. as an ancillary to another primary product or service (e.g. mobile phone insurance sold with smart phones, or legal expenses insurance together with other insurance products such as motor insurance). Furthermore some of the conduct of business provisions in the European insurance legislation does not apply to some of “small insurances”.(30)

In 2016 the proportion of claims rejected for lines of business such as legal expenses insurance or general liability insurance was higher compared to other types of lines of business. The rejection of claims (justified or not) or long claims processing times are traditionally one of the main triggers of consumer complaints. On the contrary the great majority of the medical expenses insurance claims in 2016 were upheld, and at relatively high speed, since very few claims remained open at the end of the year.

However health insurance complaints have also increased in several Member States, which could indicate that some consumers were not satisfied by the compensation received. One Member State also reported that the increase in the number of complaints was mainly motivated by premium increases in their health insurance policies, and another Member State referred to the growth of the health insurance market in recent years.

Source: EIOPA Solvency II Database

Motor insurance complaints have also increased when analysed at European level, although they have decreased in several Member States. The main cause of complaints in motor insurance is often reported to be claims-related; the graphic below shows the evolution of the processing of motor vehicle liability insurance claims in the EEA since 2012.

As it can be observed in figure 14, there seems to be a slight trend towards a higher proportion of claims not being accepted. This could be due to several reasons, such as a more strict definition and/or interpretation of the terms and conditions of the insurance policies by insurance undertakings. From a consumer protection perspective, it is paramount that the terms and conditions are transparently and accurately explained to consumers at the point of sale. Moreover it should be noted that the graphic is based only on the number of claims and not on the value of the claims.

As far as life insurance complaints are concerned, it is noteworthy that with-profits life insurance complaints decreased in more Member States than the other two types of life insurance products. A possible explanation for this behaviour could be that the market is shifting towards products with lower guarantees, although higher sales should not necessarily lead to consumer complaints if consumers’ rights are respected. Moreover the trend on the number of complaints is not reflected in the value of surrenders (including cancellation of policies as well contracts arriving to maturity) of life insurance policies in 2016.

(28) Nonlife insurance complaints increased in 16 MSs (BE, BG, FR, HR, CZ, EE, IE, LT, LU, NO, PL, PT, SK, SL, UK and IS), decreased in 7 (AT, DK, HU, LV, ES, SE and LI), remaining broadly unchanged for the rest (DE, HL, IT, MT, NL and RO). There is no information available for CY and FI

(29) Life insurance complaints increased in 13 Member States (AT, BE, BG, HR, IE, LU, NL, NO, PL, PT, RO, SK and IS), decreased in 14 (CZ, DK, EE, DE, FR, HE, HU, IT, LV, LT, MT, ES, SE and UK) remaining broadly unchanged for the rest (LI and SI). There is no information available for CY and FI.

(30) See Article 1 (3) of the Insurance Distribution Directive [Link]

(31) It only takes into account the claims reported in each year, i.e. not the outcome of the claims still open at the beginning of the year or the reopen claims during the year.

Source: EIOPA Solvency II Database

The fact that the value of surrenders of “other life insurance” is much smaller than the other two life insurance lines of business is probably linked to the GWP of each line of business (see figure 2) as well as a greater number of with profit and unit-linked policies arriving to maturity in 2016. However, the difference between the surrender value of unit-linked and with-profit policies is not aligned with the reported on-going practice in the market of encouraging customers to cancel / switch their guaranteed policies (e.g. with-profit) to policies with low or no guarantees (e.g. index and unit-linked). A deeper analysis over time of this data at national and insurance undertaking level together with other indicators could provide further insights.

Specifically in 2016, and similar to previous years, the great majority (80%) of consumer complaints in the insurance sector are related to non-life insurance products, as it can be observed in the figure 16.

Source: EIOPA Committee on Consumer Protection and Financial Innovation

Non-life insurance complaints accumulated 80% of the total number of complaints; the product categories “other non-life insurance” and motor insurance accumulated more than half of the total number of complaints (30% and 28% respectively), followed by “other-life insurance” (13%) and household insurance (8%). This is related to factors such the greater number of non-life insurance contracts, which at the same time commonly have a shorter maturity and a greater claims frequency.(33)

Indeed, claims-related issues are the main cause of complaints in insurance across the different product categories, as can be observed in figure 17; such complaints are typically related to claims handling issues such as delays, refusal of claims, insufficient compensation etc. Mis-selling /advice related issues is the main cause of complaints in some MSs for some life insurance products. For more niche products such as mobile phone insurance there is little complaints information available at NCAs.

Source: EIOPA Committee on Consumer Protection and Financial Innovation

(32) Does not include complaints data from FI,NL and FR. In the case of FI insurance undertakings reported the complaints data based on their current internal classifications which rendered their comparison impossible.

(33) By claims frequency for this report is the number of claims occurred in a given period.

4. NCA consumer protection activities

Different types of consumer protection activities are regularly performed by NCAs in their respective jurisdictions in order to safeguard the interest of consumers. Some of these activities aim to supervise that the distribution of insurance products complies with the applicable legislation (e.g. via on-site inspections or in-depth thematic reviews about a concrete topic or resolution of complaints), which may lead to the imposition of administrative or pecuniary sanctions in case of non-compliance.

Other consumer protection activities seek to foster the financial literacy of consumers (e.g. publication of financial booklets), and others consist in updating or developing the regulatory framework (e.g. new legislative acts, guidelines, opinions etc.). In 2016 the 25 NCAs that participated in EIOPA’s survey reported 65 consumer protection activities addressing one or multiple products and/or topics. (34)

Somewhat half of the reported activities directly or indirectly aimed to ensure that consumers receive adequate information about the insurance product they purchase. These activities seek to prevent some of the situations seen in the previous section where consumers misunderstood / were not aware of the characteristics and terms and conditions of the insurance product they had purchased.

Claims management issues is also a common topic addressed by consumer protection activities in the insurance sector, bearing in mind that this is the main cause of consumer complaints. Ensuring that consumers receive high-quality advice is also important to ensure good consumer outcomes, particularly as regards complex products which might be difficult to understand for an average consumer.

Figure 19 shows that despite the fact that consumer complaints have decreased in several Member States, NCAs continue to closely monitor the life insurance sector. Indeed consumer complaints are not the only risk indicator that NCAs use to monitor the markets. Moreover the deep transformation that the sector is experiencing in recent years requires NCAs to be especially vigilant.

Within the non-life insurance sector, motor insurance is the product category that is subject to the most oversight by NCAs. However it should be borne in mind that NCA activities are often cross-sectoral and do not address exclusively one product (e.g. complaints handling guidelines or financial education initiatives). The following section contains some examples (i.e. it is not an exhaustive list) of consumer protection activities undertaken by NCAs in 2016.

(34) NCAs reported the most relevant activities undertaken during 2016 but this does not represent an exhaustive list of all the consumer protection activities undertaken by the NCAs that participated in the survey. Some of the activities reported were confidential so they have not been included in the report.

Source: EIOPA Committee on Consumer Protection and Financial Innovation

Source: EIOPA Committee on Consumer Protection and Financial Innovation

4.1. Non-life insurance

The Irish NCA launched a thematic review to analyse the settlement of private motor insurance damage claims (excluding personal and bodily injury). In general, firms had adequate claims management systems and procedures, however, some issues were identified such as poor communication with claimants and delays in settling and paying the claims.(35)

Also in the area of motor insurance, the Spanish and Italian NCAs requested insurance undertakings in their respective jurisdictions to adequately justify the claim settlement offers or the refusal of to pay compensations, namely by mentioning the facts on which the decision is based (e.g. vehicle examinations, witnesses, black box results, legal medical examinations, etc.).

In 2016 the Czech NCA supervised the selling of ancillary products and services (e.g. road assistance services) with MTPL insurance. While in most cases consumers were allowed to opt-out voluntarily of these services, some potentially problematic cases were identified where the pre-contractual information provided to the consumer about these services were not appropriate and needed to be enhanced.

Since the generalisation of complementary health insurance for all salaried workers in France in 2013, the target market shrunk and the competition amongst health insurance professionals increased. The marketing channel predominantly used in this sector - door-to-door and phone selling - may sometimes lead to consumer detriment, especially for vulnerable consumers. The French NCA is closely monitoring the developments in the market and has started a series of dedicated on-site inspections regarding insurance undertakings and intermediaries’ selling practices of health insurance. (36)

Source: Slovenian Insurance Supervision Agency (37)

In Slovenia the NCA published a household insurance brochure with the aim of encourage the awareness and a better understanding of these types of products by the Slovenian population. The brochure provides information about the purpose of household insurance, key information that consumers need to pay attention when concluding the contract, common rights and obligations of the contracting parties etc.

In Romania in 2016, the Association for Insurance Promotion (APPA) organized in 3 national campaigns (2 on road safety and a third on financial education) in 2016. The first activity brought into debate a multitude of risks affecting drivers, from alcohol consumption and tiredness to using the mobile phone, while the second one focused on road dangers during the cold season. The household insurance campaign addressed among other issues some safety tips in case of an earthquake.

While the number of Payment Protection insurance (PPI) complaints is relatively low in Lithuania, last year the NCA supervised the selling practices of PPI products in view of the rapid growth of this market. The review concluded that consumers receive adequate information about the characteristic of the insurance product, coverage and terms and condition. However consumers are not offered the possibility to choose a different policy other than the one proposed by the lender, which may impact the rates and fees applied.

The Slovak NCA is also discussing how to strengthen consumer protection in the sale of PPI products with the national banking and insurance trade associations. In Slovakia, PPI products are currently sold by banking institutions through group insurance contracts, which commonly provide lower levels of consumer protection than individual insurance contracts.

In 2016 Italian NCA started to publish a list on its website with the names of the companies ranked by the number complaints received. This initiative aims to enhance market transparency, providing information to the public about the quality of services offered by the undertakings and at the same time incentivise insurance undertakings to enhance the customer care.(38) The list has already prompted the attention of the board of directors and top management of firms, stimulating intervention on the root causes of complaints.

In view of the increasing penetration of digital technologies in the insurance sector, several NCAs are increasing their activities in this area. This is the case of the Dutch NCA, which has started a thematic work to assess how undertakings’ duty of care is impacted by digital and (semi) automated services, and also what does it mean for supervisory authorities (e.g. is there is a need or not to supervise algorithms or influential third-parties such as software developers?).

Also in the area of digitalisation, the French NCA has recently issued a recommendation on the use of social media for marketing purposes in the financial sector. (39) Going forward, the Hungarian NCA is also going to pay special attention to ensuring that customer’s data qualifying as insurance secrets are treated as such, preventing, among other things, transfers of such data to unauthorised third parties. (40)

(35) Thematic Inspection of Motor Insurance Claims Damage, Central Bank of Ireland, February 2017 [Link]

(36) La Revue de l’Autorité de contrôle prudentiel et de résolution, page 15, ACPR, January 2017, [Link]

(37) Household insurance brochure, Slovenian Insurance Supervision Agency, December 2016, https://www.a-zn.si/wp-content/uploads/L4_AZN_brosura_Premozenjsko_zavarovanje_FINAL.pdf

(38) https://www.ivass.it/pubblicazioni-e-statistiche/statistiche/reportistica-reclami/index.html

(39) Recommendation on the use of social media for marketing purposes, ACPR - Banque de France, November 2016, [Link]

(40) Financial Consumer Protection report, Hungarian National Bank, March 2017, [Link]

In 2016, the UK NCA also published its assessment of the use of Big Data in retail non-life insurance, where it concluded that Big Data is producing a range of benefits for consumers by transforming how consumers deal with firms, encouraging more innovation in products and services and streamlining parts of the customer journey. However, it also found some concerns regarding the impact that enhanced risks segmentation could have for consumers with higher risk profiles, and also regarding the use of non-risk based price optimisation practices.(41)

4.2. Life insurance

Last year the Austrian NCA reviewed how insurance undertakings were implementing the new legal provisions introduced in 2015 aiming to enhance the information and transparency requirements of life insurance products (e.g. advertisement with regard to guarantees). The review concluded that the new requirements were generally fulfilled, and consumers were receiving higher quality information.

In Italy, the NCA has carried out a thematic review on dormant policies.(42) In Italy the rights arising from life insurance policies are barred after 10 years, when the sums are assigned to a public Dormant Accounts Fund. There is also a private service offered by the Italian trade association ANIA to help locate (upon request) potential dormant policies. In order to reduce the number of consumers losing their acquired rights, the NCAs has formally proposed to the Government granting insurers access to residency registers and make a periodic consultation of such registers mandatory.

The Norwegian NCA published a circular summarising the main findings of its assessment of the underlying investments in unit-linked life insurance products conducted last year. The NCA concluded that Norwegian firms do not offer complicated underlying investments in their unit-linked products compared to other Member States, although found some areas of improvements as regards the information provided to customers, including regarding the need to inform them when the insurance undertaking receives kickbacks from management companies.(43)

The new Insurance Act that entered into force in Poland in January 2016 has introduced a maximum surrender fee of 4% of the withdrawal amount in unit-linked life insurance contracts. The Polish NCA has also issued a recommendation (in the form of “comply-or-explain”) introducing new transparency requirements in the sale of unit-linked life insurance products such as the need to inform consumers about benefits received in connection with the placement of funds in a given fund, including “kick-back” bonuses.

In the Czech Republic in mid-2016 the NCA launched a thematic project to raise awareness and assess the level of readiness of insurance undertakings selling unit-linked life insurance product to implement the upcoming requirements of the PRIIPS Regulation. Due to the postponement of the application date of the Regulation the Czech NCA has also postponed its activities in this regard.

In the Netherlands, new binding standards for professional competence of financial advisors were introduced in 2016.(44) The Estonian NCA also published new guidelines / soft laws aiming to enhance the quality standards of the contractual information that consumer receive when concluding life and non-life insurance contracts.(45)

The Hungarian NCA introduced the “Ethical Concept” initiative for life insurance in order to enhance the consumer protection standards in the sector. The initiative resulted in an improvement of the sales practices of life insurance products; for example, it has been observed that some of the new life insurance products now count with a more transparent cost structure, and also the cost levels are lower due to the maximized TKM (Total Cost Indicator) levels.

(41) Feedback Statement, Call for Inputs on Big Data in retail general insurance, Financial Conduct Authority, September 2016 [Link]

(42) IVASS Report on dormant policies, August 2017 (https://www.ivass.it/consumatori/azioni-tutela/indagini-tematiche/documenti/2017/Report_investigation_dormant_life.pdf?language_id=3). Dormant policies are policies not claimed by the beneficiaries of a deceased insured person (often due to unawareness of the existence of such policy), or savings policies which, upon maturity, were not claimed for various reasons.

(43) Circular on the underlying investments in unit linked life insurance products, Finanstilsynet, March 2017 [Link]

(44) Professional competence standards for financial advisors, Financial Supervisory Authority (AFM), [Link]

(45) Guidelines on information requirements of insurance contracts, Estonian Financial Supervision Authority, November 2015 [Link]

5. Stakeholder interviews

Maria Aranzazu del Valle

Secretary General of UNESPA and Chair of EIOPA’s

Insurance and Reinsurance Stakeholder Group

Maria Aranzazu del Valle is the Chair of EIOPA’s Insurance and Reinsurance Stakeholder Group (IRSG). She is the Secretary General of the Spanish Insurance Association (UNESPA) since 1996. She is also an active member of other insurance industry associations including the Federation of Interamerican Insurance Undertakings (FIDES), the Global Federation of Insurers Associations (GFIA) and Insurance Europe.

What are in your opinion the most important developments that are taking place in the insurance sector?

Firstly, consumers are becoming more and more demanding. At the same time, risks are changing. For example, as a result of the increasing digitalization of our society new challenges are emerging such as cyber risks. Technological developments like autonomous vehicles, drones or robots also present important changes for the sector. Other developments linked to our society as a whole are also relevant such as ageing population, climate change or terrorism, just to name some. The insurance industry is constantly adapting to this new reality.

What do today’s consumers demand and how is the industry adapting to these new demands?

Consumers’ needs are more than ever at the core of the insurance business. Insurers should face nowadays an environment where clients are very demanding: they ask for very specific services and expect very fast responses. Besides that, mobile devices and social media are the new communication channels between the industry and its customers, something that is specially the case for the millennials.

However, in spite of all these changes, traditional clients deserve and demand traditional treatment as well. Therefore, insurers should handle both business models at the same time. Only those players that are able to adapt will continue to be relevant on the long run.

The interest rates continue to be at historic lows and, at the same time, people increasingly live longer. How are long-term investors such as life insurance undertakings adapting to this situation?

On the regulatory side, there have been positive developments, for instance regarding the treatment of infrastructures in Solvency II. However, Europe’s insurers hold the view that more has to be done if long-term products are to remain attractive for customers to buy and companies to offer. The industry should maintain its role as a long-term provider of (pension) products and, in turn, as a long-term investor.

Many customers appear to still want and value simple long-term products that offer guarantees and stable returns. Insurers are therefore trying to find modern ways to offer these guarantees, profit sharing and smoothing products.

In the case of Spain, most of products sold in 2016 (93%) were guaranteed products, both with-profit and guaranteed fixed interest rate products. Barely a 7% of total life premiums and technical provisions in 2016 corresponded to Unit-Linked products, where the risk is borne by the policyholder. It is clear that the use of one of the measures of the LTG package (Matching adjustment) is allowing Spanish insurance undertakings to keep on providing long term guaranteed life insurance products.

Cyber risks represent a threat or an opportunity for the insurance sector?

From the regulatory point of view, cyber risk could be a threat as it is relatively new insured phenomenon in most of Europe. In fact, market maturity differs greatly from one Member State to another.

This could make it difficult to devise an approach at European level to contribute to the aim of developing Europe’s cyber insurance market, especially in the field of standards and harmonization. Policymakers may not properly understand the way cyber insurance works and this could result in an unwanted action at EU level, such as imposing compulsory insurance for cyber risks in an effort to increase awareness and protect businesses. Compulsory measures may back-fire, so one must think very carefully before implementing them.

From the business angle we are facing an opportunity in cyber risks, as long as a precondition prevails: insurers should have access to the data gathered by the competent authorities as a result of a cyber incident under the requirements set by the GDPR and NIS Directive. If this criteria is met, the insurance industry will be able to underwrite cyber risks while gaining better knowledge of the prevention and being able to promote prevention and mitigation measures.

In your opinion, which is the main challenge and the opportunity for the industry and consumers arising from digitalisation?

The IRSG recently contributed to the European Commission’s Fintech consultation on this issue.

Regarding its potential benefits, IRSG members agreed that the development of technology applied to insurance can bring increased efficiency and reduced costs to the benefit of consumers. For example: sensor technologies, such as health monitoring devices and vehicle black-boxes allow a much deeper profiling of the customer, thus allowing an individual approach towards the risk. Such tailored insurance policies and more personalised premiums can reduce the cost for low risk policy holders that abide to proper behaviour (i.e. careful driving) and lifestyle (i.e. healthy diet and exercising). Such preventive actions improve both the span and the quality of life of the policyholder, while reducing the cost of claims for insurers.

The IRSG noted certain range of risks and concerns too. These risks need to be monitored and any gaps in regulation addressed. As an example, InsurTech could lead to lower protection for consumers if it is not regulated and supervised properly. Likewise, possible discrimination of privacy-minded consumers, unwilling to give private information, must be prevented.

In 2018 PRIIPS, IDD and the GDPR will start to be applied. How will these new legislative acts affect the insurance sector?

It is too soon to assess the impact of these projects as the markets are still waiting to know the national implementation measures.

In any case, the aim of the PRIIPs Regulation to enhance consumer protection and comparability of PRIIPs is very much welcome by all stakeholders. For example, in the future, retail investors in the EU will receive an information document containing the key features of the PRIIPs in the form of a Key Information Document (KID). Nevertheless, some examples of duplicative requirements can be found, including duplication of pre-contractual information between the Packaged Retail and Insurance-based Investment Products (PRIIPs) Regulation and the Solvency II Directive, and disclosure of costs and charges between the PRIIPs Regulation and Insurance Distribution Directive (IDD).

In practice, this means that consumers risk receiving twice the same type of information, but in a different wording and format. This will only confuse consumers and move them away from the possibility to take informed financial decisions according to their demands and needs, in spite of the fact that this was the initial objective of the PRIIPs Regulation. The provision of high-quality rather than high-quantity information is a basic principle of consumer protection. The disclosure of too much information is counterproductive and has the effect of limiting consumers’ ability to make appropriate decisions that satisfy their needs when comparing and purchasing products.

Concerning the GDPR, it will also enter into force next year so maybe it is premature to analyse its impact. To strike the balance between innovation and consumer protection will be key anyway.

What do you think should be the role of insurance supervisory and regulatory authorities in today’s digital economy?

InsurTech is something that begun as a hype but it is gradually becoming a reality. InsurTech is still very much in development with very little data or real experience on which to draw conclusions at this stage. While it is too early to consider new regulation at this stage, steps can be taken to encourage innovation while ensuring that strong consumer protection is maintained. In addition to this, ongoing monitoring is needed to identify evidence of material new risks, gaps in regulation or potential barriers created by regulation.

Similar to the IRSG, I fully support the Commission’s three core principles on this area: technology-neutrality, so that the same rules are applied to traditionally-sold products and services as those sold digitally and so ensure innovation, suitable customer protection and a level-playing field. Second, proportionality so that the rules are suitable for different business models, size and activities of all regulated entities. However, it is important to note that providing proportionality does not mean compromising consumer protection. Third, improve integrity to ensure transparency, privacy and security for consumers.

Christian van der Bosch

Co-Founder and Managing Director at Liimex (46)

In September 2016 Christian van der Bosch co-founded Liimex, a B2B insurance broker based in Hamburg, Germany. The value proposition of this InsurTech start-up turns around the digitalisation of the brokerage business, allowing its customers to conveniently access all their insurances in one same user-friendly platform online. It pro-actively manages its client accounts through the automation and digitalisation of communications and processes.

Why did you decide to enter the insurance business?